Important update — On March 31, 2026, the Department of Education changed how PSLF Buyback payment amounts are calculated for SAVE plan borrowers. The department will no longer use the SAVE plan formula to calculate buyback amounts. Instead, amounts will be based on IBR, PAYE, or ICR formulas — which are significantly more expensive. For example, a borrower who would have owed $4,300 under the SAVE formula may now owe $12,800 under IBR. If you have a pending buyback application, your agreement amount may be higher than you expected.

You’ve put in 10 years of public service. You’re close to forgiveness — maybe just a few months short — and then you find out that a stretch of deferment or forbearance doesn’t count. PSLF Buyback exists to fix that. It lets you pay a lump sum equal to what your income-driven payment would have been during those missing months, and they count toward your 120. Done right, it can unlock forgiveness you’ve already earned. Done wrong or ignored, it could cost you months or years of additional payments. This guide walks you through exactly how PSLF Buyback works, how to apply, and what to watch out for in 2026.

What Is PSLF Buyback?

PSLF Buyback lets borrowers retroactively convert months spent in eligible deferment or forbearance into qualifying PSLF payments. As long as you held a qualifying public service job during those months, you can make a lump-sum payment equal to what your income-driven repayment (IDR) plan payment would have been — and those months count toward the 120-payment total required for forgiveness.

New to PSLF? Before diving into buyback, get the full picture at PSLF Basics and Fine Print.

Who This Helps

Buyback is designed for borrowers who:

- Have 120 months of certified qualifying employment but are short of 120 qualifying payments

- Lost months to deferment or forbearance — including the COVID-19 payment pause (March 2020–September 2023) or the SAVE plan administrative forbearance

- Need immediate forgiveness: You can only use buyback if the additional months will result in forgiveness of your loans.

SAVE plan borrowers: If you were one of the 7+ million borrowers in the SAVE payment pause before it ended on March 10, 2026, those months are not automatically qualifying. Buyback is the only way to convert them — but only once you’ve reached 120 months of qualifying employment.

If you’re still years away from 120 payments, buyback isn’t available yet. But track your deferment/forbearance months carefully so you’re ready when the time comes.

Why It Matters

PSLF forgiveness is permanently tax-free at the federal level — there’s no expiration on that benefit. For most borrowers, the math is decisive: a borrower with 8 months of forbearance and a $75 IDR payment can buy back those months for $600 and walk away with their entire remaining balance forgiven. The only caveat: buyback only makes sense if it directly results in your forgiveness. If you still need many more qualifying payments, keep making them and revisit this when you’re close.

Who Is Eligible for PSLF Buyback

Quick Eligibility Reference

| Criteria | Eligible? | Notes |

| Direct Loan with outstanding balance | ✅ | Must still owe money on your loans |

| FFEL or Perkins Loan | ❌ | Must consolidate into a Direct Loan first. Consolidation uses a weighted average for PSLF counts and does not reset to zero, but you cannot buy back months from before the consolidation loan’s first disbursement date. |

| Sufficient certified qualifying employment | ✅ | You must have enough certified employment so that buying back the months would bring you to at least 120 qualifying payments. |

| Deferment/forbearance months with qualifying employment | ✅ | You must have worked for a qualifying employer during those months. |

| Loans already paid off, forgiven, or discharged | ❌ | Not eligible. |

| Months before a consolidation loan’s first disbursement | ❌ | Not eligible for PSLF buyback. |

Full Eligibility Checklist

You must meet all of the following:

- You have a Direct Loan with an outstanding balance (not paid off, discharged, or forgiven).

- You have certified qualifying public service employment.

- The months you want to buy back were in eligible deferment or forbearance (in-school deferment and grace periods do not qualify).

- Buying back those months would bring you to at least 120 qualifying payments.

You are NOT eligible if:

- You have FFEL or Perkins Loans not yet consolidated into a Direct Consolidation Loan

- The months you want to buy back are from before your consolidation loan’s first disbursement date

- Your loans are already paid off, forgiven, or discharged

Consolidation Warning

As of September 2024, consolidation uses a weighted average of your qualifying payment counts rather than resetting to zero. The formula is based on each loan’s balance and payment history, meaning larger loans carry more weight.

If your largest loan has fewer qualifying payments, consolidation can reduce your overall count.

Important for PSLF Buyback: Months that occurred before your consolidation loan’s first disbursement date are not eligible for buyback.

If you are close to 120 qualifying payments and considering PSLF buyback, review your payment history carefully before consolidating.

July 1, 2026 Consolidation Deadline: If you consolidate your loans on or after July 1, 2026, you will lose access to all legacy income-driven repayment plans (IBR, PAYE, ICR, and SAVE). Your only income-driven option will be the new Repayment Assistance Plan (RAP), which may result in higher monthly payments for many borrowers. If you’re considering consolidation for PSLF purposes, doing so before July 1, 2026 preserves significantly more repayment plan options. This restriction applies to any consolidation or new Direct Loan borrowing on or after that date.

Which Months Can You Buy Back?

One of the most common questions about PSLF Buyback is: “Can I buy back COVID-19 forbearance months?” COVID-19 payment pause months already count as $0 qualifying PSLF payments if you certify employment. Buyback is only relevant if your tracker incorrectly lists them as ineligible.

✅ Eligible Deferment and Forbearance Types

These months qualify for buyback, provided you had qualifying employment during each one:

- COVID-19 payment pause (March 2020 – September 2023)

- SAVE plan administrative forbearance

- Financial hardship deferment

- Medical or dental internship/residency deferment

- Cancer treatment deferment

- Active military duty deferment

- AmeriCorps service deferment

- Teacher Loan Forgiveness forbearance

- Local or national emergency forbearance

- PSLF application processing forbearance

- Pending borrower defense forbearance

- Administrative forbearance due to repayment plan changes

Pro-Tip on the COVID Pause: While technically eligible, the COVID-19 payment pause already counts toward PSLF as $0 qualifying payments. You only need to submit a PSLF Form certifying your employment for those years to get credit for free. Do not pay for a buyback on these months unless your StudentAid.gov tracker specifically lists them as “ineligible.”

❌ Months That Are Never Eligible

Regardless of your employment, these statuses cannot be bought back:

- In-school deferment (The most common reason for denial—see note below)

- Grace periods

- Default

- Bankruptcy

- Total and Permanent Disability monitoring period

⚠️ The “In-School” Trap: Many public servants work full-time while pursuing a graduate degree. If your loans were placed in In-School Deferment during that time, those months are strictly ineligible for buyback. You can only get credit for those months if you explicitly requested to waive the deferment at the time you were in school. If you didn’t waive it then, you cannot “buy it back” now in 2026.

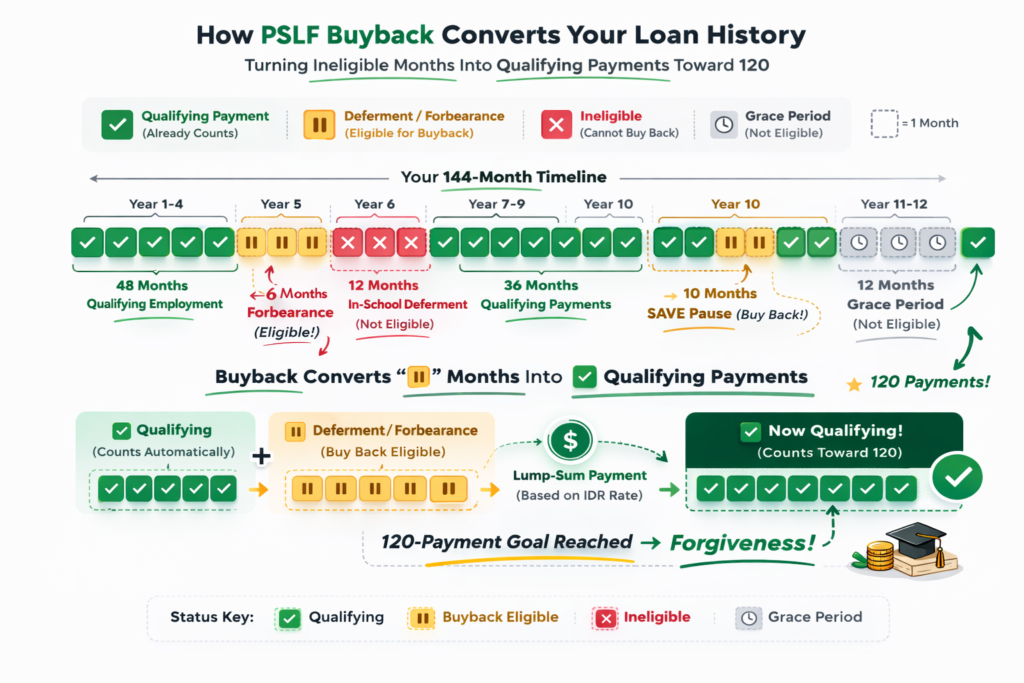

Timeline Visual

Think of your loan history as a row of months. Buyback converts ⏸ months into ✅ months:

How Is PSLF Buyback Calculated?

Your buyback cost is based on what your monthly payment would have been during the months you’re converting. The Department of Education determines this based on available repayment and income data — not on how long the period lasted.

Scenario A: You Were on an IDR Plan at the Time

For forbearances/deferments under 12 months:

Your monthly buyback amount is the lesser of:

- The IDR payment immediately before the deferment/forbearance period, or

- The IDR payment immediately after the period

Example: If your payment was $50 before a 6-month forbearance and $70 after, your buyback rate is $50/month.

For continuous forbearances/deferments 12 months or longer:

The Department of Education will require tax returns and family size documentation for each affected year to manually calculate what your IDR payment would have been. If you do not provide documentation within the required timeframe (typically 30 days), the calculation defaults to the 10-year Standard Repayment Plan amount — which is usually much higher.

⚠️ Important for SAVE forbearance borrowers: The SAVE litigation pause that began in July 2024 has already exceeded 12 months. If you’re buying back SAVE forbearance months, expect to provide tax documentation for manual calculation rather than relying on the “lesser of two payments” rule.

Sherpa Note

March 31, 2026 Calculation Change: The Department of Education announced it will no longer use the SAVE plan repayment formula to calculate PSLF Buyback amounts, even for borrowers who were involuntarily placed in SAVE forbearance. Per updated DoE guidance: ‘If the start or end date for the period of deferment or forbearance that is being bought back is on or after July 1, 2024, then the amount required to buy back that period of time cannot be based on the SAVE Plan formula.’ Instead, buyback amounts will be calculated using IBR, PAYE, or ICR formulas. Since SAVE payments were significantly lower than other IDR plans, this change could triple the cost for some borrowers. Nearly 88,000 borrowers with pending applications are affected.

Scenario B: You Were Not on an IDR Plan (or Income Must Be Reconstructed)

If you were not on an IDR plan during those months — or if the Department needs to reconstruct your income — your payment will be calculated manually.

You may be asked to provide:

- The calculated IDR amount (based on your income at the time), or

- The 10-year Standard Repayment Plan amount

You’ll be given a limited window (often around 30 days) to submit this documentation. If you do not provide it, the calculation may default to the 10-year Standard Repayment Plan amount — which is usually higher.

The Payment “Floor”

Your final buyback amount will be the lower of:

- Tax returns

- Family size information

- Income documentation for each relevant calendar year

Special Case: $0 Payment → Automatic Forgiveness

If your income at the time would have resulted in a $0 IDR payment, your buyback agreement will reflect $0 owed. No payment is required.

However, you must still submit a PSLF Buyback request and complete the process. Forgiveness is not triggered until your request is reviewed and approved.

Calculation Examples

| Scenario | IDR Payment | Months | Total |

| 6 months medical deferment | $50 | 6 | $300 |

| 10 months SAVE litigation pause | $150 | 10 | $1,500 |

| Not on IDR | $0 | 8 | $0 |

⏱ 90-day deadline: Once you receive your buyback agreement, you have 90 days to make payment. Miss it and you’ll need to restart the entire process.

How to Apply for PSLF Buyback: Step-by-Step

Step 1: Certify All Qualifying Employment

Use the PSLF Help Tool on StudentAid.gov to certify every period of qualifying employment — including the months you were in deferment or forbearance. If your employer during those months isn’t certified yet, do that first. Your request will not move forward without it.

Step 2: Identify the Months You Want to Buy Back

Log into StudentAid.gov and review your PSLF payment tracker. Look for months recorded as deferment or forbearance during periods when you were employed at a qualifying organization. Note exactly which months you need to convert to reach 120.

Step 3: Submit Your Request via PSLF Reconsideration

Go to the PSLF Reconsideration page on StudentAid.gov. Choose “Public Service Loan Forgiveness (PSLF) Reconsideration” and select “PSLF Buyback” as your request type.Include this exact language in your request:

“I have at least 120 months of approved qualifying employment, and I am seeking PSLF or TEPSLF discharge through PSLF Buyback. Please assess my eligibility for PSLF Buyback.”

Copy it carefully — this specific language is required for correct processing.

Step 4: Receive Your Buyback Agreement

Watch your email. Once reviewed, you’ll receive a buyback agreement outlining exactly how much you owe and which months are being converted. Review it carefully — if the amount looks wrong, see the denial/miscalculation section below before paying.

You have 90 days from the date of this email to make payment. The clock starts when it’s sent, not when you open it.

Step 5: Make the Lump-Sum Payment

The offer email will contain a specific link or instructions (often via Pay.gov) to make your payment. Do not simply pay your servicer (like MOHELA) through your normal monthly portal, as it may not be coded correctly as a “Buyback” payment. You must pay the full amount in a single transaction within the 90-day window.

Step 6: Confirmation and Forgiveness Processing

Once the payment is processed, your PSLF Payment Tracker will update. Final discharge can take an additional 60–90 days after the payment is made. Any regular payments you made during this waiting period will be automatically refunded after your balance hits zero.

Tips for a Smooth Process

- Screenshot everything — forms submitted, confirmation screens, emails received. The process spans multiple portals and documentation protects you if anything gets lost.

- Watch for the 90-day clock — it starts from the date the agreement email is sent, not opened.

- Don’t pause payments — continue your regular monthly payments until forgiveness is processed.

- Certify employment first — missing employment certification is the most common reason requests stall or get denied.

- Check your “Spam” folder — The buyback offer comes from the Department of Education, not your servicer. Many borrowers reported missing their 90-day window because the official email was flagged as junk.

What Happens After You Submit: Realistic Expectations

⚠️ Backlog alert: As of March 31, 2026, nearly 88,000 PSLF Buyback requests are pending. Some borrowers who submitted in late 2024 are still waiting — over a year later. This is not a reason to delay; submitting sooner puts you earlier in the queue. But don’t count on a specific forgiveness date until you have a confirmed agreement in hand. For the latest figures, see our Student Loan News & Updates 2026

Here’s what the process looks like after submission:

- No live status dashboard — updates come by email only. Check your spam folder and keep your StudentAid.gov email address current.

- Continue making payments throughout the entire waiting period. Stopping early can complicate your account status.

- Overpayment refunds — if you continue making regular monthly payments while waiting for your buyback to be processed (which is recommended), you will likely pay for months 121, 122, and beyond. Once your buyback is finalized and your account hits zero, any regular payments made after your 120th month will be automatically refunded by the Department of Education.

⚠️ Program stability note: PSLF Buyback was created in 2023 by regulation, not legislation — meaning its rules can change without an act of Congress. That is no longer a hypothetical warning. In 2026 alone: the SAVE plan was permanently struck down on March 10, the buyback payment calculation methodology was changed on March 31, and new PSLF employer eligibility restrictions are set to take effect July 1, 2026. The core PSLF program remains intact — it was established by statute and cannot be eliminated without an act of Congress — but the regulatory details around buyback have already shifted once this year. If you are eligible now, submit sooner rather than later.

What If Your Buyback Request Is Denied or Miscalculated?

Denials happen — most often due to employment certification gaps, ineligible loan types, or servicer errors. If your request is denied or your agreement amount looks wrong, you can submit for reconsideration. Before resubmitting, gather your employment certification records, loan payment history, and all correspondence as supporting documentation.

For a full walkthrough of your options:

Practical Scenarios

Scenario 1: On IDR, 6 Months in Forbearance

Maria is a public school teacher with 114 qualifying payments. She had 6 months of financial hardship forbearance with an IDR payment of $50/month before the pause.

She certifies employment for those 6 months, submits a buyback request, and receives an agreement for $300 ($50 × 6). She pays within 90 days. Those 6 months convert to qualifying payments, bringing her total to 120. Forgiveness processes.

Scenario 2: Not on IDR, Deferment Spanning Two Tax Years

James took medical deferment for 10 months straddling two calendar years. He wasn’t on an IDR plan, so the Department of Education requests his tax returns for both years.

His calculated IDR payment based on income: $120/month. Total buyback: $1,200 ($120 × 10). His remaining loan balance is $80,000 — buying back those months for $1,200 is clearly worthwhile.

Scenario 3: Pre-Consolidation Months Are Off the Table

Sarah consolidated her FFEL loans into a Direct Consolidation Loan in 2015. She has 115 qualifying payments since consolidation and wants to buy back months from 2013–2014 — before the consolidation.

Those months are not eligible. Only months after her Direct Consolidation Loan’s first disbursement date can be considered. She needs 5 more qualifying payments the traditional way. This is one of the most common points of confusion about PSLF Buyback — pre-consolidation months cannot be bought back.

Note: While Sarah can’t ‘buy’ these months back, they may have already been added to her count for free if they met the criteria for the one-time IDR Account Adjustment that occurred through 2025. If they weren’t added then, they are not eligible for PSLF buyback after consolidation.

Key Takeaways: Your PSLF Buyback Checklist

Run through this before submitting:

- ✅ You have Direct Loans with an outstanding balance

- ✅ You have enough certified qualifying employment so that buying back the months will bring you to at least 120 payments

- ✅ You’ve identified the specific deferment/forbearance months you need

- ✅ Those months fall under eligible deferment/forbearance types

- ✅ You’ve estimated your buyback amount (IDR payment × number of months)

- ✅ You’re prepared to make a lump-sum payment within 90 days of your agreement using the specific link (often Pay.gov) in your offer email.

- ✅ You’ve submitted via PSLF Reconsideration selecting “PSLF Buyback” with the required buyback language

- ✅ You’re watching your email and continuing regular payments until forgiveness is confirmed

Sign up for our newsletter to get updates on federal student loan changes, tips, and PSLF.

Additional Resources

- PSLF Basics and Fine Print — Start here if you’re newer to PSLF

- How to Recertify Your IDR Plan — Useful for understanding how your buyback payment is calculated

- TEPSLF vs. the Limited Waiver — Understand which program you’re actually pursuing

- Federal Student Loan Consolidation: A Common and Costly Mistake — Essential reading before consolidating

- Parent PLUS Loan Options — For Parent PLUS borrowers navigating PSLF

- What to Do If Your PSLF Application Is Denied

- How to Fix PSLF Rejections and Errors

FAQs About PSLF Buyback

No. The buyback amount must be paid as a single lump sum within 90 days of receiving your agreement via the specific link provided in your offer email (usually Pay.gov).

As of early 2026, realistically expect to wait many months after submission before receiving your buyback agreement. The backlog exceeds 86,520 requests. After you pay, forgiveness processing adds additional weeks. Treat the timeline as open-ended until you have a confirmed agreement.

PSLF forgiveness is permanently tax-free at the federal level — not a temporary provision, not expiring in 2026. Most states follow the federal exemption, but Mississippi currently taxes PSLF forgiveness at the state level. Check your state’s rules or consult a tax professional.

You don’t need to be currently employed at a qualifying organization. The requirement is that you had 120 months of qualifying employment in the past, and that you held qualifying employment during the specific months you want to buy back.

Parent PLUS loans have a more complicated PSLF path — they typically need to be consolidated into a Direct Consolidation Loan first and are only eligible for certain IDR plans. The TEPSLF vs. Limited Waiver article covers eligibility nuances, and Parent PLUS Loan Options goes deeper on the consolidation path.

About the Author

Pedro Gomez is the new Student Loan Sherpa and a Certified Financial Planner™ with over a decade of experience helping clients navigate complex financial decisions. He is the founder of Global Financial Plan, where he writes about international living, geoarbitrage, and strategies for retiring young, and also leads Brickell Financial Group, a registered investment advisory firm focused on accelerating financial freedom.

Pedro is the architect behind the “12 Levels of Financial Freedom” framework and blends student loan strategy with long-term planning, tax efficiency, and investing. His work is especially geared toward upwardly mobile professionals, entrepreneurs, and those looking to design a life beyond the default path.

Pedro is available for strategy sessions and press inquiries.