The fine print says that many borrowers with FFEL student loans are not eligible for the Covid-19 forbearance and 0% interest rate. However, there is a way to convert FFEL loans to gain eligibility.

The federal interest and payment freeze only applies to “federally held” student loans. FFEL loans are federal student loans but not federally held, so many borrowers are still charged interest. Fortunately, federal direct consolidation could fix this issue. Unfortunately, federal direct consolidation may be a mistake for some FFEL borrowers.

Today we will cover how to get federal loans eligible for the 0% interest rate. I will also explain why the interest break might still be a mistake for some borrowers.

Converting FFEL Student Loans into Federal Direct Loans

Federal Family Education Loan (FFEL) Program Student Loans are federal student loans. However, a third-party usually owns the debt. Hence the distinction between federally held and federal student loans.

Federal Direct Consolidation transforms FFEL debt into federal direct debt. During the consolidation, the federal government pays off the FFEL loans, and the debt is replaced with a new federal direct loan.

Prior to the student loan interest freeze, borrowers used this process to gain eligibility for the Public Service Loan Forgiveness Program. Today, the same steps mean a payment forbearance and 0% interest.

The Federal Direct Consolidation Process

The federal direct consolidation process is provided exclusively by the Department of Education.

The application is fairly simple. The Department of Education estimates that most borrowers complete the process in about 30 minutes.

Borrowers can expect the following basic steps:

- Completion of the initial application. This is the part that takes half an hour.

- The Department of Education calculates and makes arrangements for the final payoff of the original loans. Borrowers don’t need to take any action during this step.

- Funds from a new federal direct consolidation loan are used to pay off the old loans. This is the step that eliminates the FFEL loans and creates a new federally held loan.

- Borrowers start repayment on the new federal direct consolidation loan. As a federally held loan, borrowers will qualify for the Coronavirus deferment and 0% interest rate.

Important Note: While this process sounds simple, it has major consequences. Paying 0% interest until October is a great perk, but consolidation may be a huge mistake. Borrowers should understand the consequences of consolidation before starting the process.

The Validity of Direct Consolidation to Qualify for 0% Interest

I usually don’t like to inject myself into these articles.

However, this is one topic that readers may view with a bit of skepticism. I know I would.

I can say that I personally borrowed FFEL loans when I attended law school. Long before the Covid-19 pandemic, these loans were consolidated into a federal direct consolidation loan. My loans qualified for the payment and interest freeze.

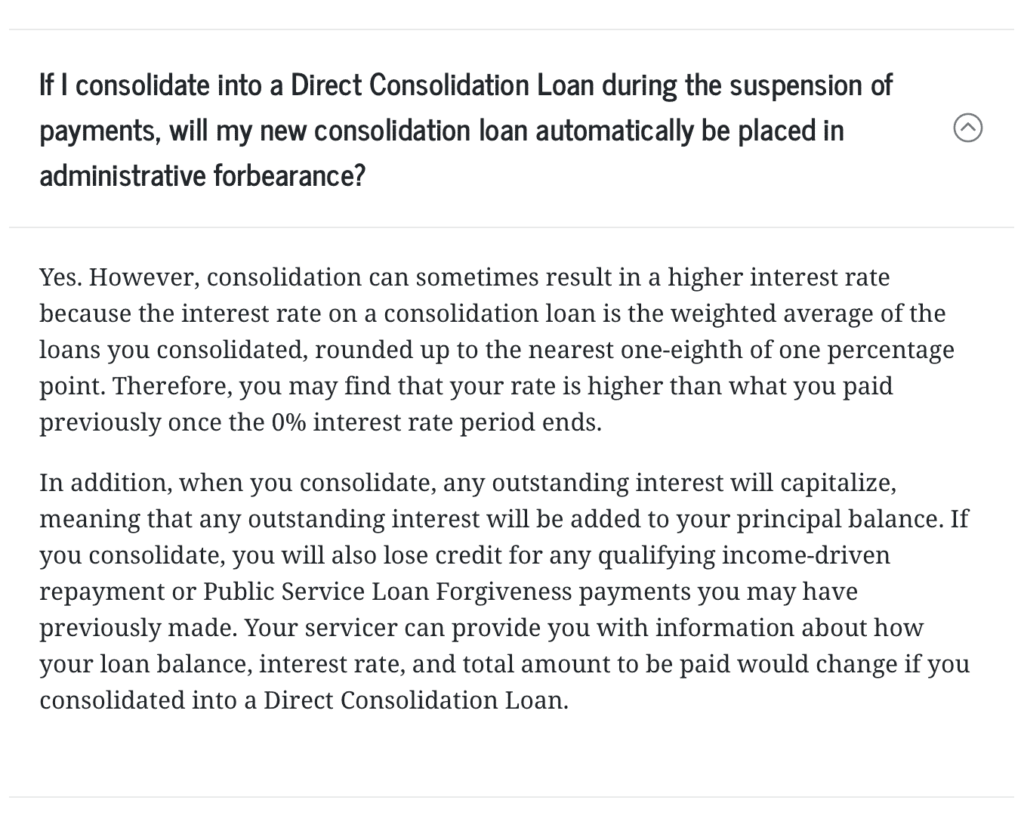

The Department of Education has stated the following on consolidation and 0% interest:

When is Federal Direct Consolidation a Mistake?

Borrowers should understand that federal direct consolidation isn’t a tiny loophole to exploit for 0% interest.

Consolidation eliminates old loans and creates a new loan. The consequences may devastate some borrowers.

In a worst-case scenario, a borrower may be approaching qualifying for student loan forgiveness on an income-driven repayment plan. By consolidating, this borrower starts the forgiveness process at the beginning. In this instance, a temporary break from interest would not justify wasting years of payments that would have counted towards forgiveness.

Borrowers must weigh the benefit of the temporary relief against the progress that consolidation erases.

Raising the stakes even higher is the fact that there is no way to undo a loan consolidation. Once the process is complete, there is no going back.

Some borrowers may have also accumulated significant uncapitalized interest on their loans. The consolidation process is one of the ways that federal interest capitalizes.

Borrowers on the fence should carefully discuss their options with their loan servicer. Reviewing the Student Loan Sherpa Federal Consolidation Guide may help prepare for this conversation.

Next Steps:

- Talk to your servicer about federal direct consolidation and the consequences for your loans.

- Start the Federal Direct Consolidation Application.

About the Author

Student loan expert Michael Lux is a licensed attorney and the founder of The Student Loan Sherpa. He has helped borrowers navigate life with student debt since 2013.

Insight from Michael has been featured in US News & World Report, Forbes, The Wall Street Journal, and numerous other online and print publications.

Michael is available for strategy sessions and to respond to press inquiries.