Many borrowers find choosing between PAYE and REPAYE challenging. Pay As You Earn (PAYE) and Revised Pay As You Earn (REPAYE) don’t merely sound similar — many of the key terms of these plans are identical.

However, despite the many similarities, there are times when one repayment plan is significantly superior to the other.

When comparing these two plans, we can’t crown a winner as there isn’t a “best” option between REPAYE or PAYE. Some borrowers will be better off with REPAYE, while others should choose PAYE. Today we will look at the circumstances that impact the decision between these two plans.

The Similarities Between PAYE and REPAYE

Before jumping into the differences, it is worth taking a moment to point out the many ways in which these plans are similar or even identical. Both plans are Income-Driven Repayment (IDR) plans. The Department of Education designed the IDR plans to keep monthly payments affordable.

For many borrowers, the monthly payments on PAYE and REPAYE will be identical. Both plans require borrowers to pay 10% of their monthly discretionary income towards their student loans.

Sherpa Tip: Curious about your monthly payments?

Check out the Department of Education’s Loan Simulator to get an estimate on your monthly payment for the various repayment plans.

Both REPAYE and PAYE qualify for multiple student loan forgiveness programs, including Public Service Loan Forgiveness (PSLF). Additionally, the rules regarding taxes on forgiven debt are the same for both plans. Some forgiveness options don’t result in a tax bill; others do.

Finally, borrowers are allowed to switch between the two plans. Enrollment in PAYE or REPAYE does not cause any commitment to a particular plan.

Why Married Borrowers Prefer Pay As You Earn

A significant difference between PAYE and REPAYE is how the plans treat spousal income.

Generally speaking, payment calculations on Income-Driven Repayment (IDR) plans like PAYE and REPAYE include your spouse’s income in the equation to determine how much you can afford to pay. This math gets complicated for borrowers who both have federal student loans, but for couples where only one person has federal loans, marriage means higher payments.

Under PAYE, if a couple files their taxes separately, spousal income isn’t included in payment calculations. Excluding this income can mean dramatically lower monthly payments.

Unfortunately, filing taxes separately does not help borrowers enrolled in REPAYE. Thus, if you are married and want to exclude your spouse’s income from your monthly payment calculations, PAYE is the better option.

Borrowers with Large Balances and Small Payments Should Pick REPAYE

REPAYE comes with a valuable interest subsidy.

Some borrowers on income-driven repayment plans have student loan balances that are growing each month. This happens when the monthly payment is smaller than the monthly interest generated by the loan.

On most IDR plans, if the monthly payment is $100, but interest charges are $150, the balance will increase by $50 each month. (Note: that extra $50 isn’t immediately added to the principal balance. That addition happens when an event triggers interest capitalization.)

The REPAYE subsidy essentially wipes away half of the “extra” interest charges each month. In our example, the borrower’s balance would grow by $25 each month instead of the full $50.

REPAYE is the only plan that offers the subsidy. If your monthly payment is small compared to the monthly interest on the loan, the REPAYE savings could be significant.

Sherpa Tip: Some suggest that the REPAYE subsidy doesn’t matter if you are chasing after PSLF because the entire balance will eventually be forgiven tax-free.

I disagree.

If things go as planned, it won’t matter. However, PSLF doesn’t always work out. REPAYE might prove to be a better choice if you have to turn to Plan B or Plan C for your student debt.

The PAYE Advantage for Graduate School Borrowers

All income-driven repayment plans come with forgiveness after making monthly payments for a specified number of years.

PAYE borrowers must make payments for 20 years, and then their remaining debt is forgiven.

Under REPAYE, forgiveness comes after 20 years for borrowers who only borrowed undergraduate loans. Those who borrowed loans for graduate school must make payments for 25 years before earning forgiveness.

Getting forgiveness five years earlier is a potentially huge advantage to PAYE.

Older Borrowers Are Stuck with Revised Pay As You Earn

Only certain student loan borrowers can sign up for PAYE. There are two age requirements to qualify for PAYE:

- Must be a new borrower as of Oct. 1, 2007 – This means if you had federal student loans on the books before Oct. 1, 2007, you cannot sign up for PAYE.

- Must receive a disbursement of a Direct Loan on or after Oct. 1, 2011 – If you stopped borrowing before October of 2011, you cannot sign up for PAYE.

Part of the reason REPAYE came into existence was to help borrowers with debt too old to qualify for PAYE. These borrowers don’t get to decide between PAYE and REPAYE.

A Final Tip on Deciding Between REPAYE and PAYE

If you have a preference between REPAYE and PAYE, be careful when you fill out your income-driven repayment application.

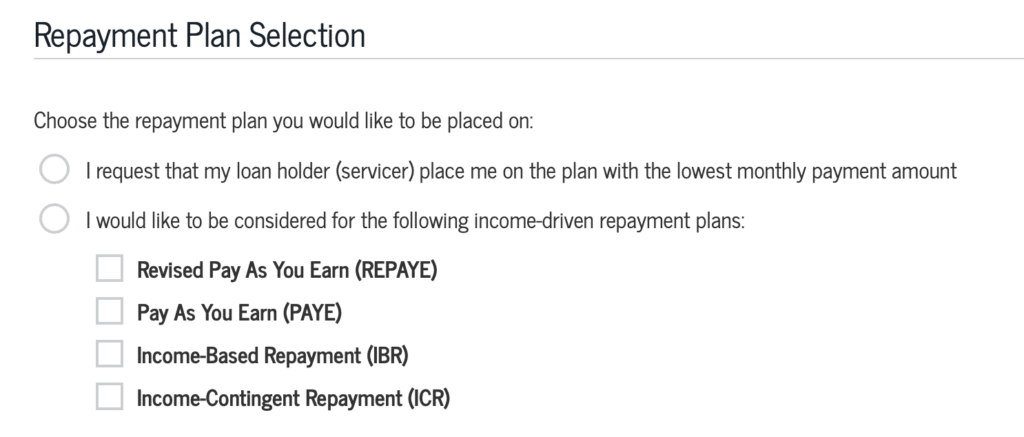

On the IDR application, borrowers will have the following choice:

Many borrowers instinctively choose the first option because they want the lowest monthly payment.

However, because PAYE and REPAYE are so similar, they often result in equal monthly payments. If a borrower has a preference between the two plans, they should specify the desired plan on their application to avoid accidentally enrolling in the wrong program.

If you are ready to sign up for REPAYE or PAYE, the application can be found here. The Department of Education estimates borrowers will need about ten minutes to complete the form.

About the Author

Student loan expert Michael Lux is a licensed attorney and the founder of The Student Loan Sherpa. He has helped borrowers navigate life with student debt since 2013.

Insight from Michael has been featured in US News & World Report, Forbes, The Wall Street Journal, and numerous other online and print publications.

Michael is available for strategy sessions and to respond to press inquiries.