Choosing the wrong repayment plan could cost you tens of thousands of dollars — or add years to your repayment timeline.

That’s not a scare tactic. It’s just the reality of how different IBR and RAP actually are. For some borrowers, IBR will be the clear winner. For others, RAP will cut their monthly payment significantly. The problem is that nobody is going to tell you which one is right for you.

That’s what this guide is for.

Quick Answer: IBR vs. RAP

Not sure which plan fits you? Here’s the short version. The detailed breakdown follows.

| Your Situation | Better Plan |

| High income (typically $80k+) | IBR |

| Low-to-moderate income (typically under $80k) | RAP |

| Close to 20 or 25-year forgiveness | IBR |

| Worried about interest growing your balance | RAP |

| Pursuing PSLF | Whichever has the lower monthly payment |

| Borrowing after July 1, 2026 | RAP (primary IDR option) |

| Married with very different incomes | Likely IBR — run the numbers |

| Have dependent children | RAP may be competitive — $50/child deduction |

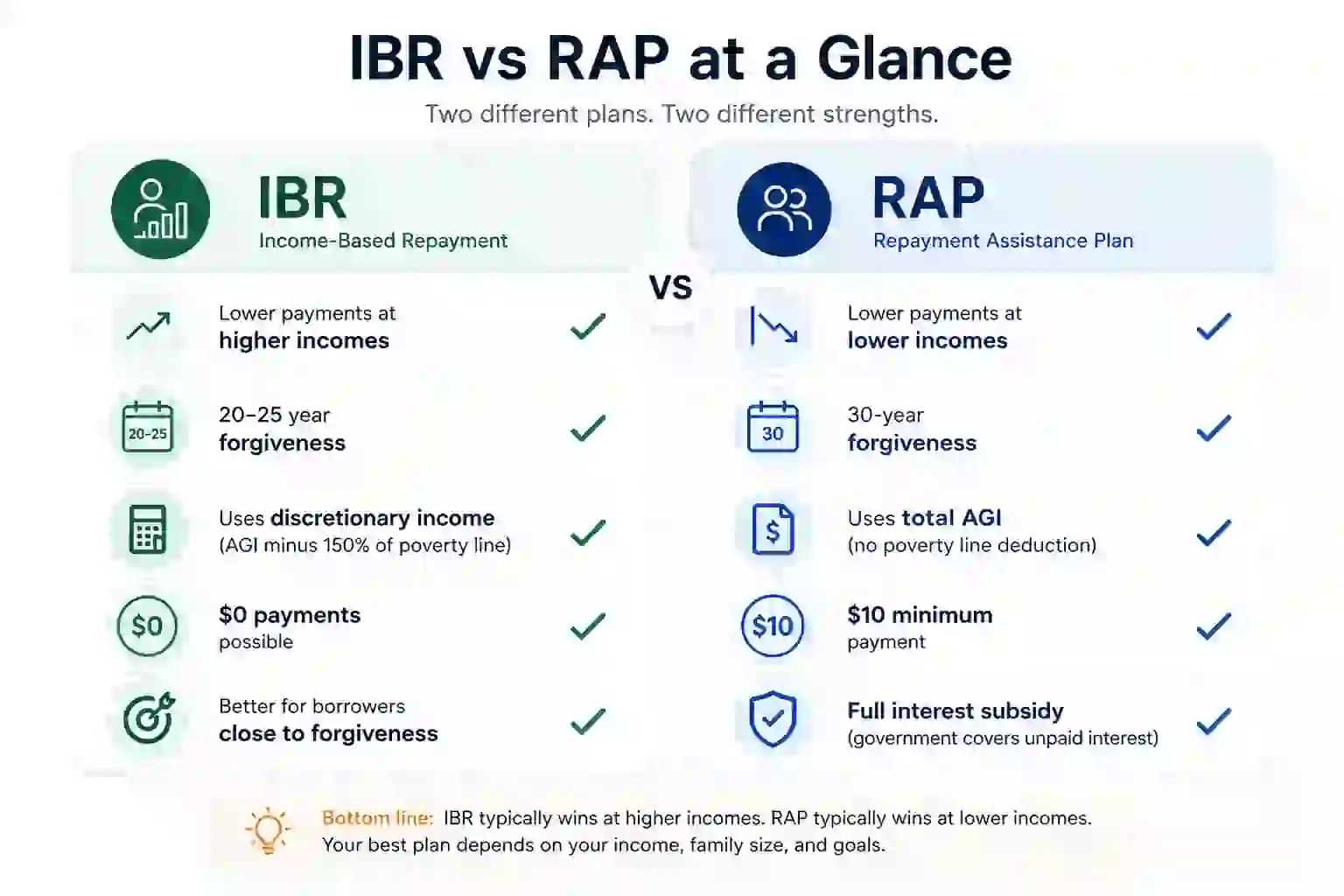

What Is IBR?

Income-Based Repayment (IBR) has been around since 2009. It ties your monthly payment to your income, not your loan balance, and offers forgiveness after 20 or 25 years.

Here’s where it gets confusing: there are actually two versions of IBR, and which one you’re on depends on when you borrowed.

- Old IBR (had an outstanding federal loan balance as of July 1, 2014): Payment is 15% of discretionary income. Forgiveness after 25 years.

- New IBR (borrowed on or after July 1, 2014, with no outstanding federal loan balance as of that date): Payment is 10% of discretionary income. Forgiveness after 20 years. The bigger win here is the lower payment rate — not the cap.

Both versions cap your payment at what you’d owe on a standard 10-year plan. And if your income is low enough, your payment could be $0.

Want to see your number? Run it through our Old IBR calculator or New IBR calculator depending on when you first borrowed.

Sherpa Note: If you take out new federal loans on or after July 1, 2026, IBR won’t be available to you. If all your loans were disbursed before that date and you don’t borrow again, IBR remains a permanent repayment option for you. There’s one critical trap though: if you take out even one new loan after July 1, 2026, all your loans could be moved off IBR and onto RAP or the Tiered Standard Plan. If you’re planning to borrow again, that decision deserves serious thought before you sign anything.

What Is RAP?

The Repayment Assistance Plan — RAP — is brand new. It was created by the One Big Beautiful Bill Act, signed into law in 2025, and it launches on July 1, 2026.

RAP is the only income-driven repayment option for borrowers taking out their first loans on or after July 1, 2026. IBR remains available only to grandfathered borrowers — those who already had an eligible loan balance before the cutoff and haven’t taken out new loans since. If you’re starting from scratch after July 2026, your choices are RAP or the new Tiered Standard Plan — a fixed-payment plan whose repayment term (10, 15, 20, or 25 years) is based on how much you borrowed.

Here’s how RAP works: instead of calculating payments based on discretionary income, it charges a flat percentage of your total adjusted gross income (AGI). The rate scales up as your income grows.

RAP also has a $10/month minimum. You will always owe at least $10, even if your income is nearly zero.

And there’s a meaningful upside: a full interest subsidy. If your monthly payment doesn’t cover accruing interest, the government covers the gap. Your balance won’t balloon while you’re making payments.

The catch? Forgiveness doesn’t come until after 30 years.

RAP also includes a Matching Principal Payment provision found in no other plan. If your on-time monthly payment reduces your principal balance by less than $50, the government makes up the difference — capped at the lesser of $50 or your actual payment amount, minus whatever principal your payment already reduced. For borrowers with smaller balances making modest payments, this guarantee of meaningful monthly principal reduction can accelerate payoff even within a 30-year timeline.

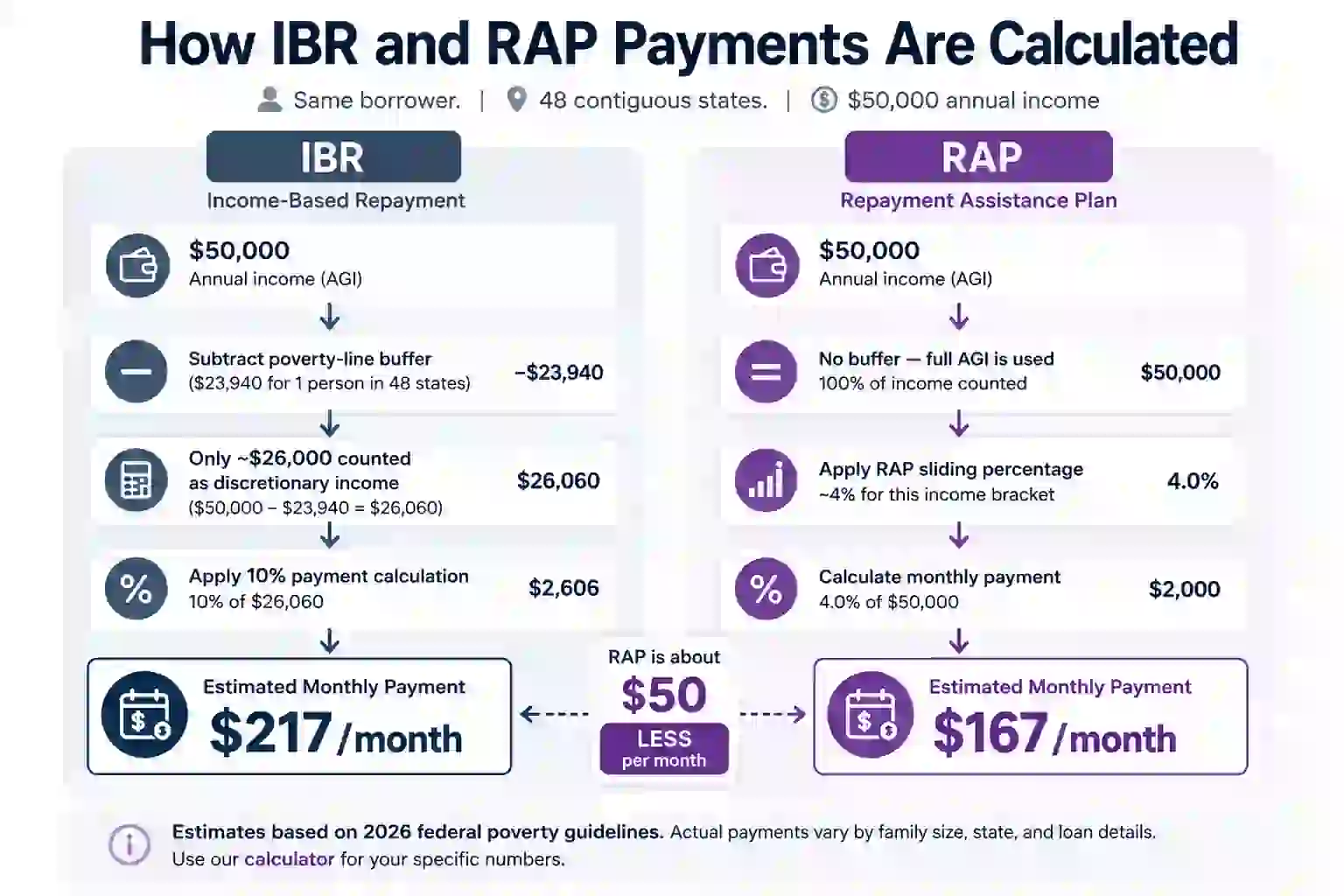

How IBR and RAP Payments Are Calculated

This is the core of the IBR vs. RAP debate — and the two plans use completely different math.

IBR: Subtracts a Poverty-Line Buffer First

IBR doesn’t charge you a percentage of your full income. It charges you a percentage of your discretionary income — that’s your AGI minus 150% of the federal poverty line. Understanding how AGI factors into your student loan payments and how discretionary income is calculated will help you make sense of why these plans produce such different numbers.

For a single borrower earning $50,000, IBR doesn’t charge you 10% of $50,000. It charges you 10% of roughly $26,000. That difference adds up fast.

RAP: Charges a Percentage of Your Full AGI

RAP skips the poverty-line buffer entirely and charges a sliding percentage of your total AGI. The rate starts small at lower incomes and scales up as you earn more.

RAP does have one deduction: for every dependent child you claim on your taxes, your monthly RAP payment drops by $50. Two kids, that’s $100/month back in your pocket. For families, this changes the comparison meaningfully. As a general rule, RAP tends to produce lower payments at lower incomes. IBR typically wins at higher incomes because the poverty-line buffer does a lot of work. But the crossover point depends on your specific income, family size, and loan balance — which is why running the actual numbers matters.

Sherpa Tip: Don’t guess. Use our RAP calculator and compare it against our Old IBR calculator or New IBR calculator depending on when you borrowed. And don’t just calculate based on your income today — RAP’s rate scales up as you earn more, so a plan that looks cheaper now could flip in five years if your income grows.

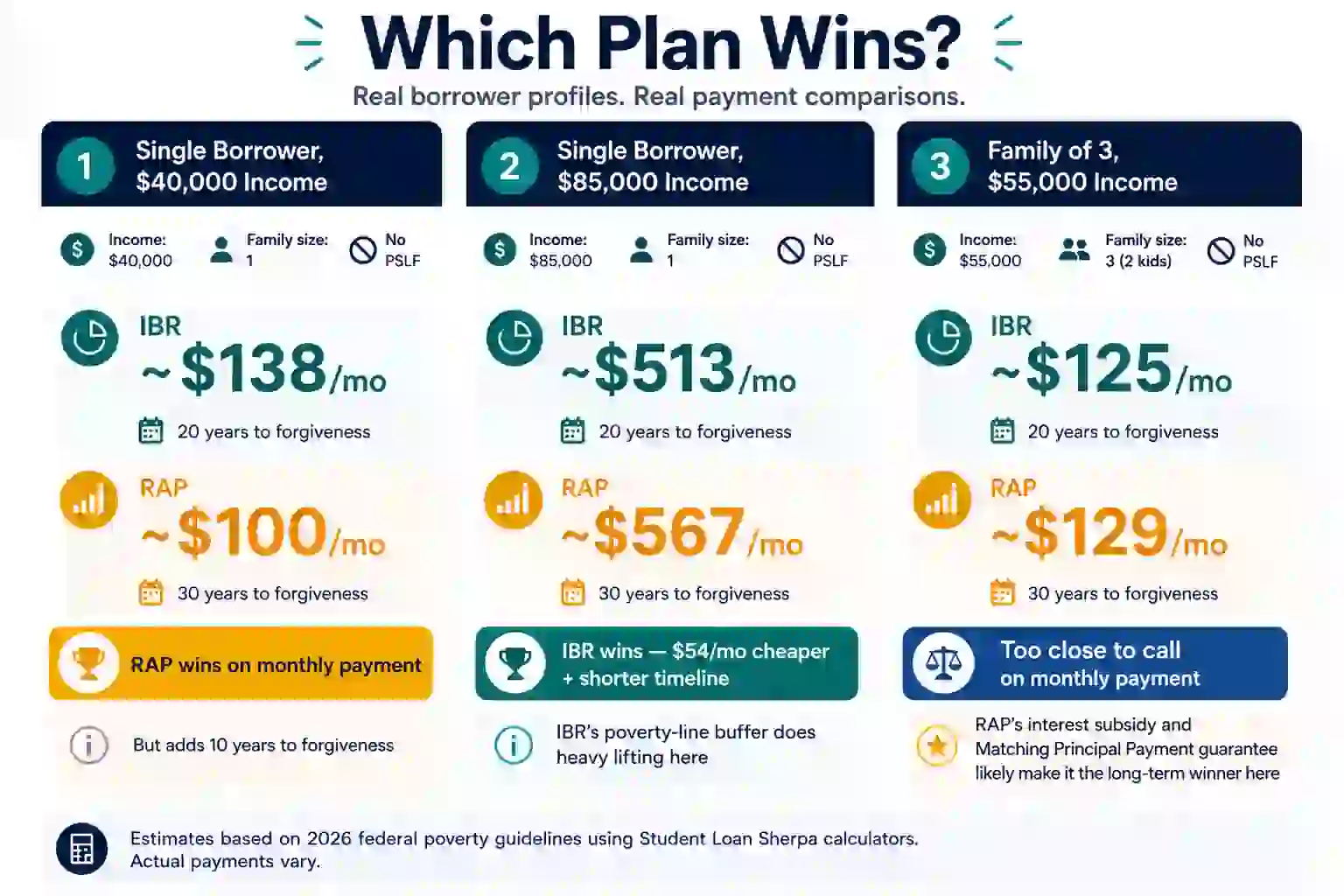

Real Numbers: Three Borrower Profiles

The infographic below shows what IBR and RAP actually produce for three common borrower situations, calculated using our own calculators. Assumptions: New IBR eligibility (borrowed after July 1, 2014), 48 states and DC poverty guidelines, no PSLF.

Profile 1: Single Borrower, $40,000 Income

IBR: ~$138/mo (20 years) vs. RAP: ~$100/mo (30 years)

Takeaway: RAP produces the lower monthly payment here — $38 less per month. But the borrower trades that savings for an extra 10 years before forgiveness. Whether that tradeoff makes sense depends on their long-term income trajectory. If they expect significant raises, RAP’s scaling percentage could flip the math over time.

Profile 2: Single Borrower, $85,000 Income

IBR: ~$513/mo (20 years) vs. RAP: ~$567/mo (30 years)

Takeaway: IBR wins clearly here. It’s $54/month cheaper and reaches forgiveness 10 years sooner. This is the high-income crossover in action — the poverty-line buffer in IBR’s formula does significant work at this income level.

Profile 3: Borrower With Two Kids, $55,000 Income

IBR: ~$125/mo (20 years) vs. RAP: ~$129/mo (30 years)

Takeaway: This one is almost a tie on monthly payments — just $4 apart. IBR technically wins, and it offers forgiveness 10 years sooner. But here’s the nuance: RAP’s full interest subsidy means that if the $129 payment doesn’t cover all accruing interest, the government picks up the difference. If this borrower is worried about their balance growing, RAP’s interest protection could tip the decision. The $4/month difference is close enough that the forgiveness timeline and interest subsidy become the real factors.

Estimates based on 2026 federal poverty guidelines using Student Loan Sherpa calculators. Actual payments vary.

IBR vs. RAP: Side-by-Side

| IBR | RAP | |

| Payment calculation | % of discretionary income | % of total AGI |

| Minimum payment | $0 | $10/month |

| Forgiveness timeline | 20–25 years | 30 years |

| Interest subsidy | Limited (subsidized loans only, first 3 years) | Full — govt covers the gap |

| PSLF eligible | Yes | Yes |

| Open to new borrowers after 7/1/2026 | No (unless no new loans) | Yes |

| Family size definition | Broad | Narrow ($50/child tax deduction) |

| Parent PLUS loans | No | No |

| Typically better for PSLF optimization | Sometimes | Often |

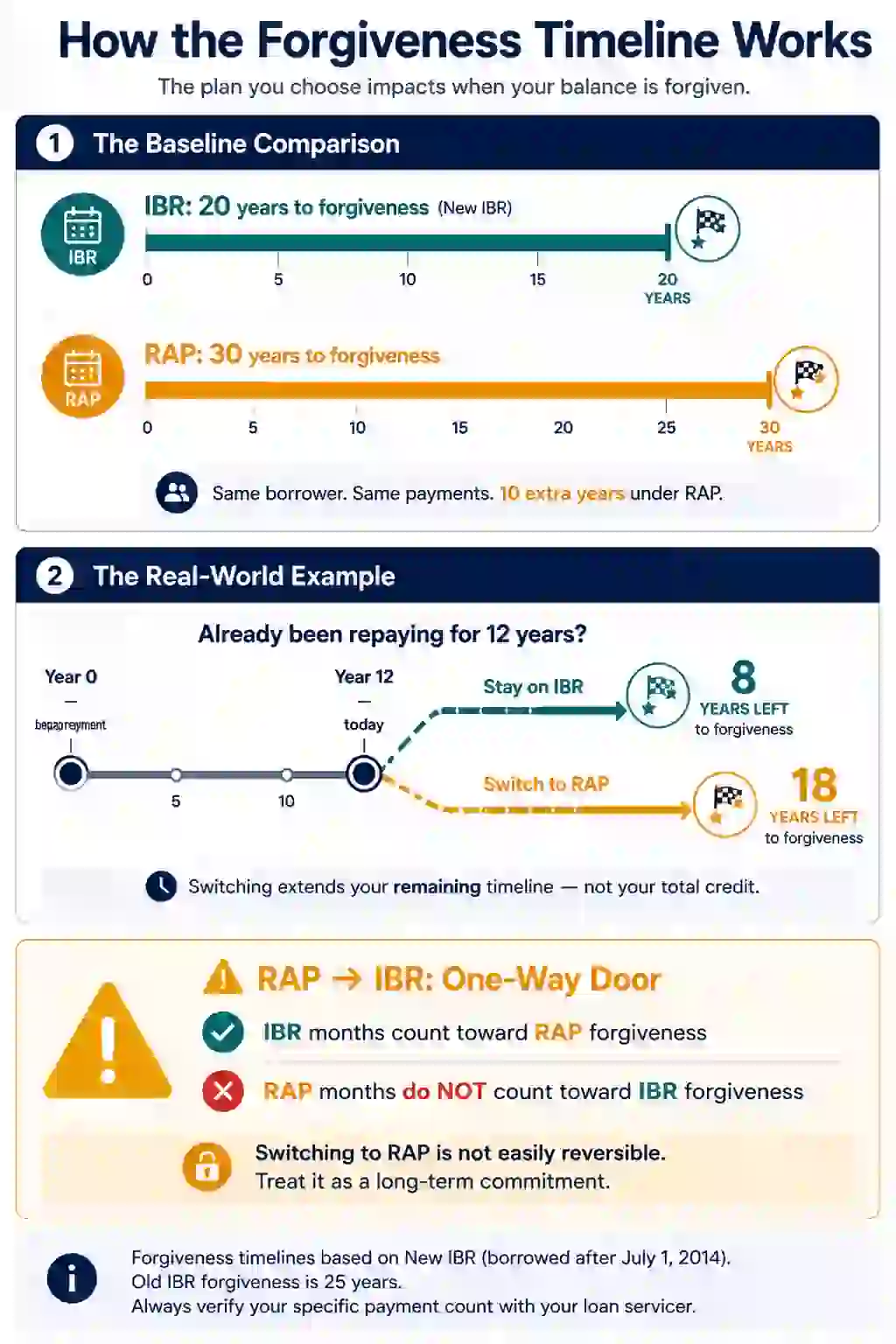

Loan Forgiveness: 20 or 25 Years vs. 30 Years

This is where IBR vs. RAP gets really important — especially if you’ve already been in repayment for a while. IBR forgives your remaining balance after 20 years (new IBR) or 25 years (old IBR). RAP forgives after 30 years. That’s a 5 to 10 year difference.

That’s worth repeating: switching from IBR to RAP doesn’t reset your clock to zero — but it does extend your forgiveness timeline to 30 years total. If you’ve already been making payments for 12 years under IBR, you’re 8 years from forgiveness. Switch to RAP, and you’ve got 18 years left.

If You Switch Plans (Without Consolidating)

If you switch from IBR to RAP, your prior IBR payment months carry over. You don’t lose the credit you’ve already built up.

But here’s the trap: this only works one way. If you later switch back from RAP to IBR — say, because you want the shorter 20-year forgiveness timeline — those months spent in RAP will not count toward IBR forgiveness. The longer you stay in RAP before switching back, the more credit you lose.

Switching to RAP is not easily reversible for forgiveness purposes. Treat it as a long-term commitment, not a trial run.

If You Consolidate to Get onto RAP

This is where it gets trickier. Your forgiveness credit becomes a weighted average across all loans in the consolidation — weighted by balance.

- If you consolidate a $50,000 loan with 10 years of credit and a $5,000 loan with zero credit, you keep most of that credit. The large balance carries the calculation.

- But flip those balances — $5,000 with 10 years of credit, $50,000 with zero — and you’ve just wiped out nearly everything you’ve built.

Sherpa Tip: If you’re considering consolidation to access RAP, run the weighted average math first. Consolidating carelessly could cost you years of forgiveness credit.

The Forgiveness Tax

The federal tax exemption for IDR forgiveness has expired. A forgiven balance may be treated as taxable income in the year it’s discharged. Make sure you’re not caught off guard by the forgiveness tax bill.

One exception: PSLF forgiveness remains tax-free at the federal level. Don’t just brace for the tax bill — plan for it. Calculate your projected liability, then open a dedicated taxable brokerage account and invest a set amount monthly in a broad index fund. A modest monthly contribution over 10–15 years, compounding the whole time, can organically build the exact war chest you’ll need when the IRS comes calling. Starting early is everything here.

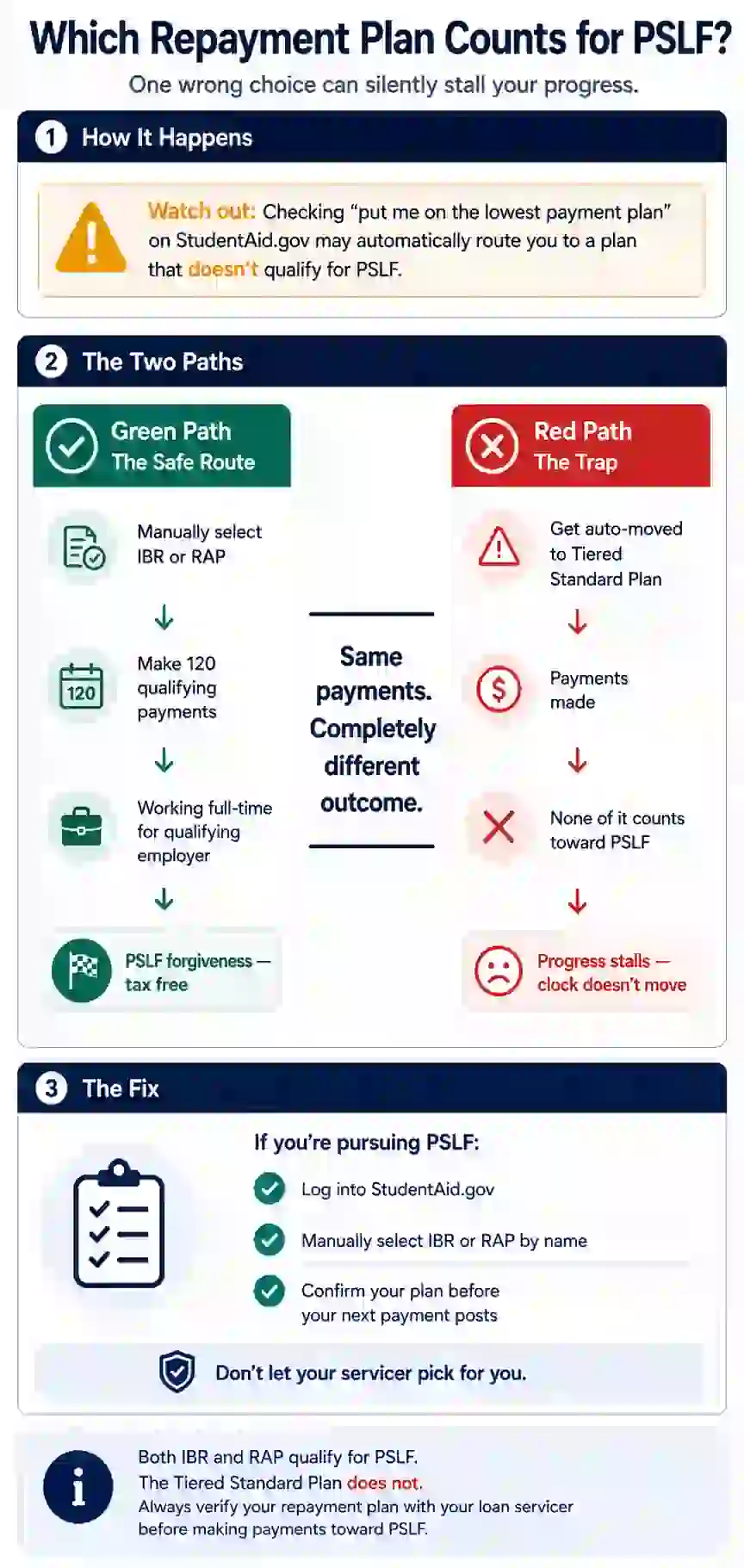

PSLF: Does the Plan You’re On Matter?

Good news: both IBR and RAP count toward Public Service Loan Forgiveness. The 10-year, 120-payment requirement didn’t change.

If you’re working toward PSLF, the plan you choose is mostly about minimizing monthly payments — since PSLF wipes the balance after 10 years regardless.

In many PSLF cases, RAP may actually outperform IBR — despite the longer 30-year forgiveness timeline. Why? Because PSLF borrowers aren’t aiming for 20- or 30-year forgiveness at all. They’re aiming for the lowest possible qualifying payment over 120 payments. That changes the math completely.

For PSLF borrowers specifically:

- A lower monthly payment typically matters more than a shorter forgiveness timeline

- Interest growth matters less, since the remaining balance is forgiven tax-free through PSLF

- The better plan is usually whichever produces the smaller required payment over the next 10 years

Example: A borrower paying $150 less per month under RAP compared to IBR could save $18,000 over a full PSLF timeline. In that situation, RAP’s longer 30-year forgiveness schedule becomes largely irrelevant — the balance disappears after 10 years through PSLF anyway.

That said, IBR still has one meaningful advantage for PSLF borrowers: stability. IBR is an older, well-established plan with a long PSLF track record. RAP is newer, and implementation details may continue evolving. For borrowers with many years left before 120 payments, that’s worth factoring in.

Sherpa Tip: For PSLF borrowers, the optimal strategy is usually simple: choose whichever qualifying repayment plan produces the lowest monthly payment while preserving PSLF eligibility. If you’re close to 120 payments, that’s the only number that matters.

Watch out for two traps that could derail your PSLF progress:

The Tiered Standard Plan Trap

The new Tiered Standard Plan — the other option created by the OBBBA — does NOT qualify for PSLF. If you’re a new borrower and get automatically moved to the Tiered Standard Plan without realizing it, those months won’t count toward your 120 payments. You have to manually switch to RAP to keep your PSLF progress on track.

The Parent PLUS Trap

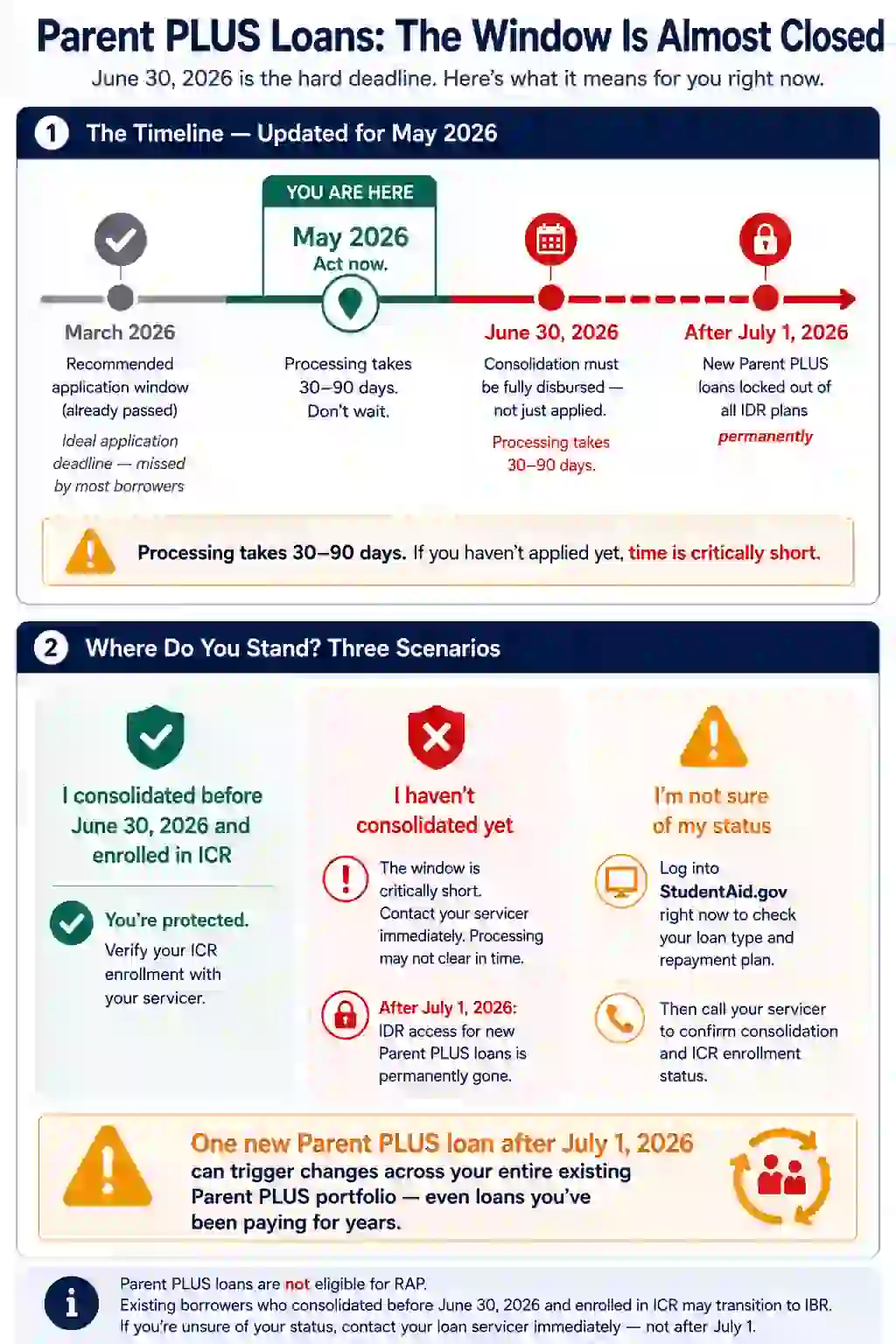

Parent PLUS borrowers face a critical two-step process with two different deadlines — and confusing them could cost you permanently.

Step 1 — Consolidation (Hard Deadline: June 30, 2026): Your Parent PLUS loans must be consolidated into a Direct Consolidation Loan, and that loan must be fully disbursed — not just applied for — by June 30, 2026. Processing takes 30–90 days, so applying in May or June is already dangerously late for most borrowers.

Step 2 — ICR Enrollment (Deadline: June 30, 2028): Once your consolidation is disbursed, you have until June 30, 2028 to formally enroll in ICR and make at least one full, on-time payment. That single payment then unlocks the option to switch to IBR, preserving your 25-year path to forgiveness.

Miss Step 1, and IDR access is permanently gone. Miss Step 2, and you lose the IBR transition window.There’s one more landmine: take out even one new Parent PLUS loan after July 1, 2026, and your existing Parent PLUS loans can be pulled onto the Tiered Standard Plan — which has no IDR forgiveness and no PSLF eligibility. One new loan can trigger changes across your entire portfolio.

For the full breakdown of deadlines and the step-by-step workflow, see our Parent PLUS loan forgiveness deadline guide.

Special Situations: When You Probably Need Help

Some situations are genuinely complicated, and the standard IBR vs. RAP comparison won’t cut it.

Married Borrowers

Both IBR and RAP allow married borrowers to file separately and exclude a spouse’s income. IBR’s real edge for married couples is the poverty-line buffer — that deduction from your income before the payment calculation kicks in does significant work at moderate income levels. One caveat for RAP filers: if you file separately under RAP, your dependent count is limited to children claimed on your individual return, which can reduce the $50/child deduction. And for either plan, filing separately has real tax costs — some OBBBA deductions don’t apply to MFS filers — so run the full tax picture before deciding. See our guide to IBR for married couples.

Parent PLUS Borrowers

Neither IBR nor RAP is available to new Parent PLUS borrowers after July 1, 2026. If you have existing Parent PLUS loans, the consolidation deadline is critical — and the deadline is disbursement, not just application. Processing takes 30–90 days, meaning experts recommended applying by March 2026. Miss this, and IDR access is permanently gone.

Note: Applications submitted in May 2026 may not disburse before June 30. Call your servicer today to assess your options.

There’s one more landmine here. Take out even one new Parent PLUS loan after July 1, 2026, and your existing Parent PLUS loans can be pulled onto the Standard Plan. One new loan can trigger changes across your entire portfolio.

High Balances

If you owe $150,000, $300,000, or more, the difference between a 20-year and 30-year forgiveness timeline — and the tax consequences — can be enormous. The math gets complicated fast. If any of these situations describe you, a one-hour conversation can save you years of uncertainty. ➤ Book a consultation with the Sherpa and we’ll work through your specific numbers together.

Who Should Choose IBR?

IBR is typically the right call if you:

- Have significant repayment credit built up and don’t want to extend your forgiveness clock to 30 years

- Earn over $80,000 — IBR’s discretionary income calculation tends to produce lower payments at higher incomes

- Expect a significant income jump in the future — IBR has a statutory payment cap. Your monthly payment can never exceed what you’d owe on a standard 10-year plan, no matter how high your income climbs. RAP has no such cap. For residents becoming attendings, or anyone on a steep income trajectory, that ceiling is meaningful protection.

- Have a complex family situation — IBR’s broader family size definition can significantly lower your payment

- Are married with uneven incomes and want to file separately to shield your spouse’s income

- Already have loans disbursed before July 2026 and want to protect your IBR access — you need to actually be enrolled in IBR before July 1, 2026. Having old loans isn’t enough protection. If you haven’t enrolled and you later take out a new loan or consolidate, you could be automatically moved to the 30-year RAP track.

Who Should Choose RAP?

RAP is typically the right call if you:

- Are a new borrower after July 1, 2026 — RAP is your primary IDR option, and for most, the only one. IBR is largely restricted to borrowers who already had a balance before July 2026. If you’re starting fresh, RAP is it.

- Earn under $70,000–$80,000 — RAP’s lower percentage rates can undercut IBR at these income levels

- Are worried about interest growing your balance — RAP’s full interest subsidy prevents negative amortization

- Are currently on SAVE, PAYE, or ICR and need to pick a new plan before those plans are eliminated in 2028

- Claim children on your taxes — the $50/child monthly reduction can make RAP competitive even against IBR’s lower base rate

Sherpa Note: If you’re currently on SAVE forbearance and trying to switch plans, watch out for a common servicer glitch. If you check the ‘put me on the plan with the lowest monthly payment’ box on StudentAid.gov, the system may automatically route you back to SAVE — which is legally blocked and phasing out. Your application will be denied. To avoid this, manually select IBR or RAP by name. Don’t let the system auto-select.

Key Deadlines You Can’t Miss

If you remember nothing else from this article, remember these dates. Too many borrowers have missed critical deadlines simply because they didn’t know the rules changed. Don’t let that be you.

| Deadline | What It Means |

| July 1, 2026 | IBR closes to borrowers who take out new federal loans on or after this date. If you haven’t borrowed anything new, you can still enroll in IBR until 2028. |

| June 30, 2026 (disbursed — not just applied) | Parent PLUS consolidation must be fully processed and disbursed by this date. Processing takes 30–90 days — experts recommended applying by March 2026. Miss this, and IDR access is permanently gone. |

| July 1, 2028 | SAVE, PAYE, and ICR are eliminated. If you don’t proactively choose IBR or RAP before this date, you’ll most likely be auto-placed on RAP. Exception: if you have loans that aren’t eligible for RAP — such as a Parent PLUS consolidation loan — the Department of Education will default you into IBR instead. Either way, don’t let your servicer decide for you. Proactively choose your plan before the deadline. |

See the full list of important student loan deadlines.

The rules are still evolving. Regulations are being finalized, court challenges are ongoing, and servicers are struggling to keep up. ➤ Join our free newsletter — we track every change and explain what actually matters for borrowers.

A Simple Way to Decide Between IBR and RAP

Still not sure? Walk through this in order.

- Run both payment estimates using our calculators — RAP and IBR side by side, based on your actual income and family size.

- Compare forgiveness timelines. How many years of credit have you already built? How many years until forgiveness under each plan?

- Estimate your income in five years, not just today. RAP’s rate scales up as you earn more — a plan that’s cheaper now may not be in five years.

- Decide how much the interest subsidy matters to you. If your balance growing keeps you up at night, RAP’s full interest coverage is a real benefit.

- If you’re close to forgiveness, model the impact carefully before switching. Extending your timeline by even five years changes the math significantly.

Bottom Line

IBR and RAP are not interchangeable. The right plan depends on your income, your loan balance, your family situation, and how many years of repayment credit you’ve already accumulated.

Here’s the short version:

- Higher income or close to forgiveness? IBR is typically the better choice.

- Lower income or new borrower? RAP is often the stronger move.

- Complicated situation? Don’t guess.

Your action for today: Run the numbers on both plans. Use our RAP calculator and compare it against our Old IBR calculator or New IBR calculator depending on when you borrowed. It takes five minutes. And model both your current income and where you expect to be in five years — RAP’s rate scales up as you earn more, so a plan that looks cheaper today could flip as your career grows. That five minutes could be worth thousands of dollars.

For most PSLF borrowers, the better plan is whichever produces the lower monthly payment — full stop. PSLF wipes your balance after 120 qualifying payments regardless of which plan you’re on, so the 30-year RAP forgiveness timeline is largely irrelevant. Both IBR and RAP qualify. The Tiered Standard Plan does not — so don’t get auto-placed there without realizing it.

You can switch from IBR to RAP, and your IBR payment months carry over. But the reverse doesn’t work the same way — if you switch back from RAP to IBR, those RAP months will not count toward IBR forgiveness. Switching to RAP is effectively a one-way door for forgiveness purposes. Treat it as a long-term commitment, not a trial run.

Don’t switch off PAYE voluntarily right now — but not because of capitalization. As of July 2023, leaving PAYE no longer triggers a capitalization event, so your accrued interest won’t suddenly get added to your principal when you switch. The real reason to stay put is strategic: PAYE sunsets in July 2028, and you have time to carefully model IBR vs RAP before being forced to decide. Use that window to run the numbers, assess your income trajectory, and switch on your terms. One important warning if you’re considering IBR specifically: switching from IBR voluntarily to another plan is one of the remaining statutory capitalization triggers. So if you move to IBR and later want to leave, make sure you’re ready to commit.

IBR — and this is one of the clearest cases where it matters. IBR has a statutory payment cap: your monthly bill can never exceed what you’d owe on a standard 10-year plan, no matter how high your income climbs. RAP has no such cap. As an attending, your RAP payment scales up with every dollar you earn. If you’re also pursuing PSLF, the calculus shifts: pick whichever qualifying plan produces the lowest payment during your remaining months toward 120. For most residents-turned-attendings on PSLF, that’s still IBR once income spikes.

If you have significant repayment history or a higher income, switch to IBR now — don’t wait. SAVE is legally blocked and every month in forbearance may not be counting toward forgiveness. One critical warning: when you apply, manually select IBR by name on StudentAid.gov. Don’t check “lowest payment” — the system may route you back to SAVE and deny your application. If your income is lower and you’re close to July 2026, it’s reasonable to switch to IBR now and re-evaluate RAP when it launches.

IBR subtracts a poverty-line buffer (~$23,940 for a single borrower in 2026) from your income before calculating your payment. You only pay 10% of what’s left — not 10% of your full income. RAP skips the buffer entirely and charges a percentage of your full AGI based on 11 income brackets, ranging from 1% at the lowest incomes up to 10% for those earning over $100,000. There’s also a $10 monthly minimum under RAP — unlike IBR, there are no $0 payment options even if your income drops to zero. That single structural difference is why IBR typically wins at higher incomes and RAP often wins at lower ones.

Yes — and it often tips toward RAP. For smaller balances, RAP’s two built-in protections become proportionally more valuable. First, the full interest subsidy: if your payment doesn’t cover accruing interest, the government waives the difference. Second, the Matching Principal Payment: if your on-time monthly payment reduces your principal by less than $50, the government makes up the shortfall — but with a specific cap. The government’s contribution is limited to the lesser of $50 or your actual payment amount, minus whatever principal your payment already covered. In plain terms: the government won’t contribute more than you paid, and won’t contribute more than $50. For a borrower whose small payment goes almost entirely to interest, this provision ensures at least some meaningful principal reduction each month. One important caveat: paying more than your required RAP payment can reduce or eliminate this benefit, since extra payments reduce principal directly — potentially pushing your payment-driven principal reduction above $50, which is the threshold that triggers the match. On RAP, paying exactly what’s billed is usually the optimal strategy.

About the Author

Pedro Gomez is the new Student Loan Sherpa and a Certified Financial Planner™ with over a decade of experience helping clients navigate complex financial decisions. He is the founder of Global Financial Plan, where he writes about international living, geoarbitrage, and strategies for retiring young, and also leads Brickell Financial Group, a registered investment advisory firm focused on accelerating financial freedom.

Pedro is the architect behind the “12 Levels of Financial Freedom” framework and blends student loan strategy with long-term planning, tax efficiency, and investing. His work is especially geared toward upwardly mobile professionals, entrepreneurs, and those looking to design a life beyond the default path.

Pedro is available for strategy sessions and press inquiries.