In most student loan reviews, I focus on terms like interest rates, repayment length, and cosigner requirements. Reviewing Stride Funding’s Income Share Agreement (ISA) presents some unique challenges.

ISAs are still in their infancy. The newness of ISAs requires me to first discuss income share agreements generally and how income share agreements compare to student loans. After that, I can review the specifics of Stride Funding.

Borrowers already familiar with ISAs can use the table of contents below to jump into the Stride specific review.

What is an Income Share Agreement?

An income share agreement is a financial product that students can use to pay for college.

The ISA is an actual contract between a lender and the borrower. Borrowers agree to pay the lender a portion of their income for a specific period of time.

The big advantage of an ISA is protection for the borrower if college doesn’t work out. If you go to school and can’t find a job, you won’t have ISA bills coming in. Similarly, an ISA protects underemployed borrowers. If you are not earning much money, an income share agreement will cost the borrower very little.

The potential downside comes if things go well after school. Borrowers with higher incomes could end up paying back much more than what they borrowed. ISAs usually provide a cap on borrower spending, but the maximum repayment can be relatively high.

Income Share Agreement Pros and Cons: Income share agreements make look and sound like student loans, but they are very different. Take a close look at all the pros and cons of an income share agreement before making any major decisions.

Getting Income Share Agreements vs. Student Loans

ISAs and student loans look very similar.

They are both tools to pay for school and have terms set by an agreement between a lender and a borrower.

Qualifying for an ISA works differently than a student loan.

- ISAs don’t really care about your credit score. Any credit check is usually done to discover major issues.

- ISAs are far more concerned with the school you attend and your area of study.

Additionally, ISA lenders are also far more concerned with your progress in school. If you are in your final year of studies, you will have a better shot at qualifying for an ISA than you would if you were in your first year.

Bottom line, the better your career prospects appear to be, the better your odds of getting an ISA.

Deciding Between an Income Share Agreement and a Student Loan

Most borrowers eligible for an ISA can also get a student loan.

Choosing between these options can be difficult. While student loan costs are fairly predictable, ISAs could cost nothing or be very expensive.

In my opinion, students should first max out federal student loan options before opting for an ISA. This is because federal loans may offer the best of both worlds. Borrowers who do well financially after school can repay the debt plus interest and be done. Borrowers who struggle have federal protections like income-driven repayment (DR) and student loan forgiveness. A federal loan on an IDR plan will function similarly to an ISA.

Things get interesting when comparing a private student loan to an income share agreement.

One way to compare options would be to project how much the ISA might cost if you are an average student with an average income at graduation.

Comparing Stride vs. Private Student Loans

The basic terms with Stride look much different than a traditional student loan:

| Stride Funding ISA | |

|---|---|

| Income Share Length | 5 - 10 Years |

| Maximum Yearly Funding | $25,000 |

| Income to be Shared | 2.0% - 15.0% |

| Maximum Total Payment | 2x Original Loan |

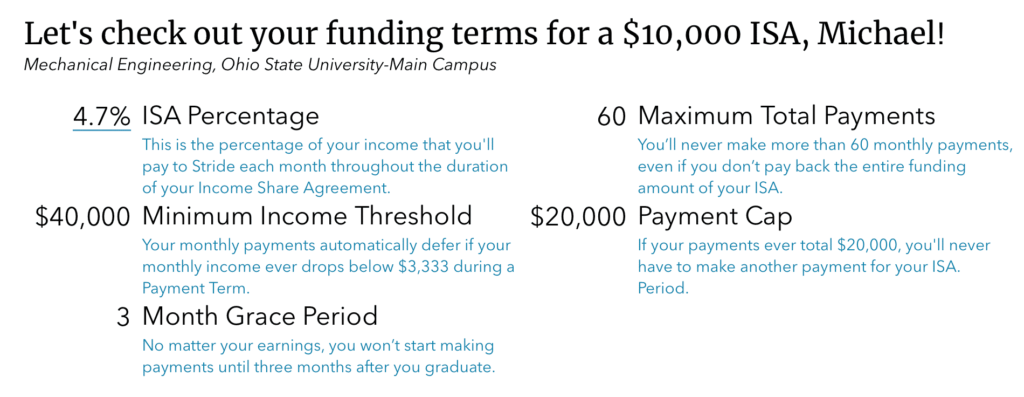

To review Stride Funding, I looked up actual income share offerings on the Stride website. I found that a third-year English major at Ohio State University would not get help from Stride. However, a fourth-year mechanical engineering student would qualify for help. Specifically, Stride would provide $10,000 of funding for school in exchange for a 4.7% income share.

Here are the terms Stride offered:

The Stride application makes it fairly easy to compare a Stride Loan to a traditional private loan.

In my example, a Stride income share and a private loan nearly break even under the following circumstances:

Graduates who earn less money or can only find private loans with double-digit interest rates will be more likely to benefit from an income share. If you can find a loan with a lower interest rate, or expect to earn more money, then a private loan might be the better option.

There are many other variables besides projected earnings and available private loan interest rates. How confident are you in your earning potential? What would you do if you couldn’t find a job? Are you more worried about the risk of not finding a job or the risk of spending more than necessary?

Reviewing the Fine Print on Stride Funding Income Share Agreements

I reached out to Stride to dig down into some of the details of the income share agreement.

I learned the following:

- Borrowers earning below the minimum income do not have to make any payments.

- Three milestones can end the income sharing requirement:

- The borrower makes 60 total payments (5 years worth),

- Ten years pass since the end of the grace period, or

- The borrower pays double the original amount borrowed.

- Determining the income to be shared can be tricky.

- Stride will use pay stubs or employment contracts to determine income.

- At the end of the year, Stride compares the borrower’s income against their tax return to make sure the borrower didn’t overpay or underpay for the previous year.

- This approach might be complicated for people with variable incomes like hourly, seasonal, or self-employed workers, but the end of year tax verification should correct overpayment or underpayment.

- Borrowers can sign away a maximum of 15% of their future income with Stride.

Due to the relative newness of ISAs, borrowers with questions should reach out to companies like Stride before signing any agreements.

Is it a Good Idea to get an Income Share Agreement with Stride Funding?

I’m genuinely torn on this issue.

For starters, I think whether or not Stride or any other ISA is a good idea will depend upon where you are in school.

Graduate Students – Grad students probably won’t benefit from an ISA due to high federal student loan borrowing limits. Unlike undergrad, where federal loans are limited, graduate students usually qualify for all the federal aid they need.

Undergrad Students – Stride is worth considering as an alternative to private loans. It could end up costing more, but an ISA offers excellent protection if the investment in college doesn’t pay off as planned.

I think Stride is best for students approaching graduation who are concerned that their private debt balances are too large. Opting for an ISA can help ensure that the private loan payments stay manageable.

Stride could also be an option for borrowers who have plenty of scholarships, grants, and federal loans but need a bit of extra cash to pay for school. Borrowing through Stride could help these borrowers avoid private student loans completely.

Finally, Stride is a great choice for borrowers who are short on funds and cannot find a cosigner. No cosigner lending is where Stride excels.

Click here to investigate Stride Funding ISA options.

About the Author

Student loan expert Michael Lux is a licensed attorney and the founder of The Student Loan Sherpa. He has helped borrowers navigate life with student debt since 2013.

Insight from Michael has been featured in US News & World Report, Forbes, The Wall Street Journal, and numerous other online and print publications.

Michael is available for strategy sessions and to respond to press inquiries.