If your employer doesn’t qualify for Public Service Loan Forgiveness (PSLF), zero of your monthly payments will count toward forgiveness. It does not matter how long you have worked there. You could make a $600 payment every single month for ten years, fully expecting an $85,000 loan balance to vanish, only to discover a technicality disqualified you from day one.

Because this government system is horribly broken, your loan servicer will never tap you on the shoulder to warn you about an employer eligibility mistake. If you want to protect your financial future, you have to verify everything yourself.

This article will help you complete a proper PSLF employer lookup using the official tool. We will cover exactly who qualifies under the shifting federal rules, how to run your search, and the precise steps you must take to lock in your progress.

Use the PSLF Employer Search Tool Right Now

Borrowers regularly spend up to an hour on hold with a servicer just to ask, “does my employer qualify for PSLF?” You do not have to endure that kind of institutional torture. Go straight to the official government tool at studentaid.gov/pslf/employer-search.

This PSLF employer search tool is the fastest way to get a baseline reading on your organization. The database shows which employers have already been vetted and approved. To run your PSLF employer search, you only need your employer’s legal name or their Employer Identification Number (EIN).

Do not rely on your HR representative for this answer. HR professionals are often just as confused by federal student loan rules as everyone else. The government database is the only source you should consult for a preliminary answer.

Sherpa Tip: The database is an excellent first check, but it is not an official confirmation of your status. Even if your organization appears with a green checkmark, you still have to submit the Employer Certification Form (ECF) to actually lock in your payment counts.

Which Employers Qualify for PSLF

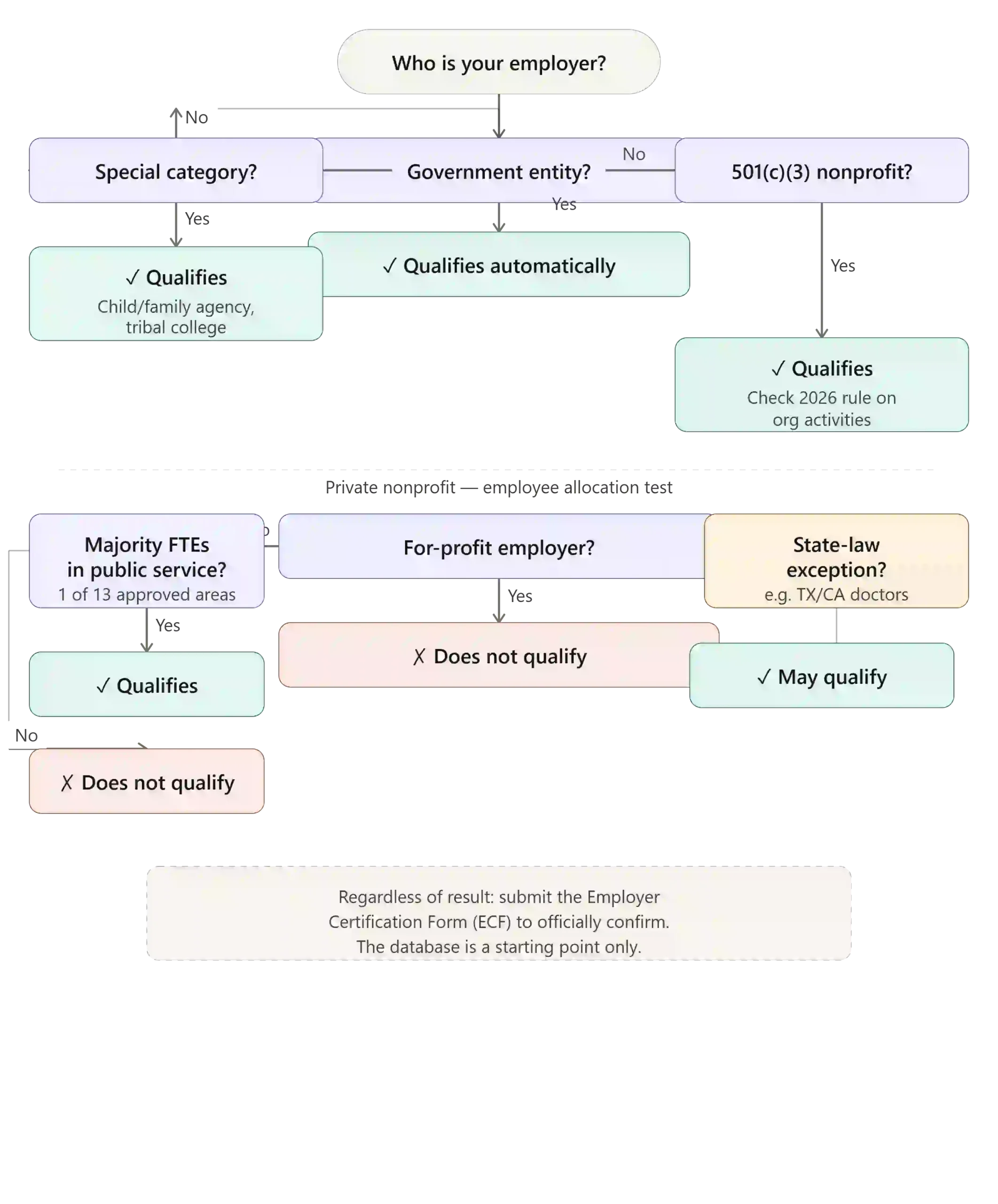

The government’s rules for PSLF qualifying employers are incredibly complex and currently undergoing massive, frustrating changes. You must pay very close attention to how your organization is legally structured.

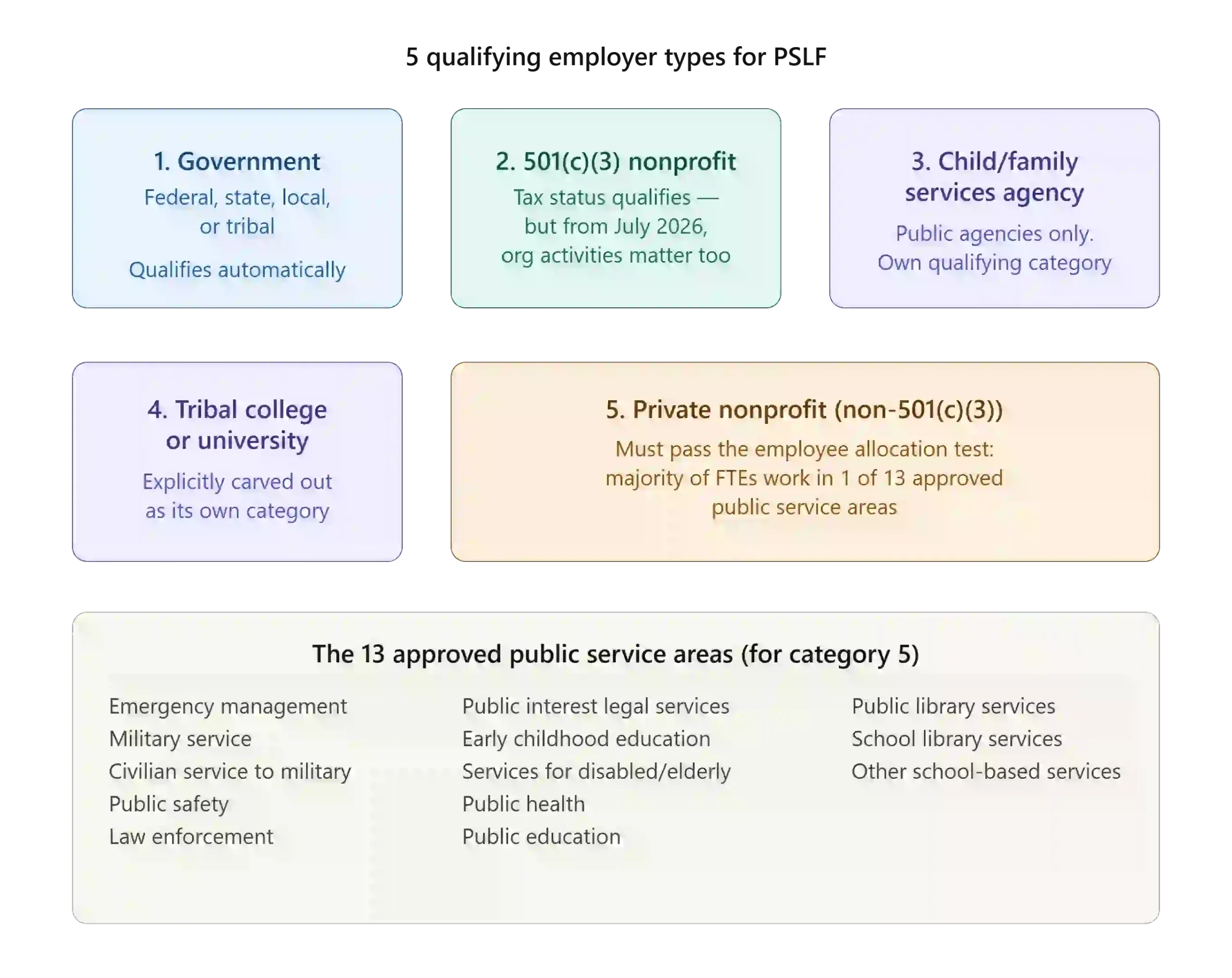

Under federal regulations, there are exactly five distinct categories of PSLF eligible employers:

- All government employers. This includes federal, state, local, and tribal government organizations. Whether you are a public school teacher, a city transit worker, or a state park ranger, all of these qualify automatically.

- 501(c)(3) nonprofits. Historically, the tax status was the only test. However, a newly finalized Department of Education rule, scheduled to take effect in July 2026, excludes organizations—including registered 501(c)(3)s—that the government determines engage in activities with a “substantial illegal purpose.”

- Public child or family service agencies. These organizations are explicitly protected as their own independent qualifying category under federal law.

- Tribal colleges or universities. This is also explicitly carved out as a unique, fully qualifying category.

- Private nonprofits. If the organization lacks 501(c)(3) status, the government uses a strict employee-allocation test. The Department of Education does not care about the organization’s formal mission statement or “primary purpose.” To qualify, the employer must devote a majority of its full-time equivalent employees to working in at least one of 13 approved public service areas.

Those 13 approved areas are: emergency management, military service, civilian service to military personnel, public safety, law enforcement, public interest legal services, early childhood education, public service for individuals with disabilities and the elderly, public health, public education, public library services, school library services, and other school-based services.

Sherpa Thought: The upcoming 2026 rule for 501(c)(3) nonprofits is a significant shift — the actual activities of the nonprofit now matter, not just its tax status. Work such as supporting undocumented immigrants, providing gender-affirming care, or advancing diversity and inclusion programs could potentially disqualify your employer. It’s worth monitoring how your organization’s activities align with the new rule, especially if your work touches any of these areas.

You must also be incredibly careful about the government contractor trap. Generally speaking, who writes your paycheck is what matters, not where you physically work.

Imagine a custodian employed directly by a qualifying hospital. Because their $40,000 salary comes directly from the hospital, that custodian qualifies. Now imagine that same custodian doing the exact same work at the exact same hospital, but employed by a third-party, for-profit cleaning company. Because a for-profit company issues their W-2, they do not qualify.

However, there is a legal exception to this paycheck rule. Under federal regulations, you can qualify if you work as a contracted employee for a qualifying employer in a position that, under applicable state law, cannot be filled by a direct employee. For example, doctors in Texas and California who are legally barred by state law from being directly employed by nonprofit hospitals can still qualify for PSLF despite being paid by a for-profit entity.

Sherpa Note: Labor unions and partisan political organizations do not qualify for the program under any circumstances. This remains true regardless of their official tax status.

How to Run a PSLF Employer Lookup Step by Step

Running a PSLF employer lookup should be simple. However, government websites are rarely user-friendly. Here is the exact path to take so you do not get derailed by a glitchy interface.

- Go directly to studentaid.gov/pslf/employer-search.

- Search by your employer’s name first. Searching by EIN is technically more precise, but borrowers don’t always have it handy.

- Understand your results. The system will tell you if your employer is “eligible,” “not eligible,” or “not found.”

- If your employer isn’t in the database, don’t assume they’re ineligible. A “not found” result often just means no one has submitted paperwork recently, so proceed directly to the ECF.

If you have a common employer name, you might need to run a PSLF EIN lookup to be completely certain. Where do you even find your EIN?

It is incredibly easy. Grab your most recent W-2 tax form and look closely at box b. That specific nine-digit number is your golden ticket for a precise search.

If you work for a publicly traded company, you can also use the SEC EDGAR lookup tool online. Just keep in mind that this SEC shortcut works for corporate entities, but it will not help you with most government agencies or smaller nonprofits.

Sherpa Tip: Always search by name first. Only use your EIN if the name search is ambiguous or throws a confusing error.

The ECF: The Only Official Verification

I cannot emphasize this enough: the online search database merely gives you a strong signal. The Employer Certification Form (ECF), submitted through the official PSLF Help Tool, is the only official confirmation recognized by the government.

Historically, MOHELA handled these reviews, which led to endless lost paperwork and inaccurate counts. Thankfully, the Department of Education overhauled PSLF servicing in July 2024 and transitioned the program entirely away from them.

MOHELA no longer updates the official tracker, so checking their old portal is useless. Today, borrowers must log directly into their StudentAid.gov account to view their qualifying payment counts and certified employment periods.

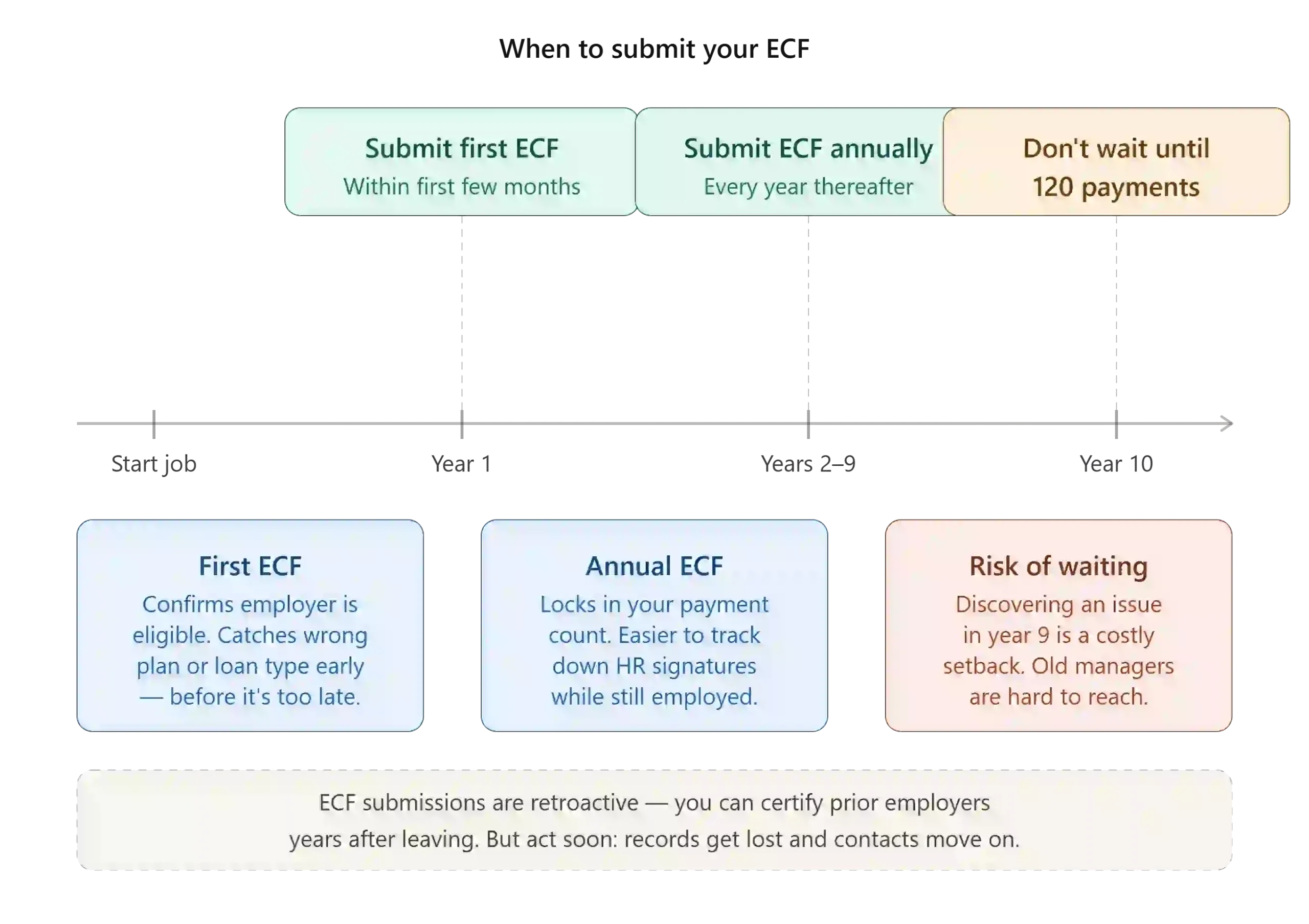

When you submit your ECF, the Department of Education reviews it, confirms your qualifying payment count, and flags if you are on the wrong repayment plan or hold ineligible loan types. Discovering you are on the wrong repayment plan during your first year is a minor speedbump. Discovering it in year nine is a $60,000 financial tragedy.

That’s worth repeating: Submit the ECF after your first few months at any qualifying employer, and annually after that. Do not wait until you’re approaching 120 payments.

This process is also fully retroactive. Prior employers can be certified years after you leave the job.

Get that paperwork signed sooner rather than later. Tracking down a former HR manager from five years ago is incredibly frustrating because businesses close, managers retire, and records get lost.

Edge Cases Worth Knowing

The student loan system is filled with stressful gray areas that trap hardworking people. Keep this tight—if your workplace falls into one of these edge cases, your path to forgiveness requires extra vigilance:

- Quasi-public entities: Organizations like state lottery corporations, public instrumentalities, and utility districts are not automatically qualifying. The ECF is the only way to officially confirm their status with the Department of Education.

- Hospitals: For-profit hospital systems do not qualify for forgiveness; 501(c)(3) nonprofit hospitals do. Always check the legal tax classification rather than relying on the hospital’s public reputation.

- Government contractors: Working at a government facility for a private, for-profit employer does not count. The only exception is if you fall under the state-law carveout for positions that legally cannot be filled by direct employees.

Sherpa Note: An ECF approval is not a legally binding guarantee. In a 2016 lawsuit, the Department of Education explicitly argued that a loan servicer’s approval letter “does not reflect a final agency action.”

This became public when four attorneys working for non-501(c)(3) organizations—such as the American Bar Association—had their previously certified employment retroactively disqualified. The issue was not the government arbitrarily changing its mind, but rather a dispute over ambiguous employer eligibility classifications. A federal judge ultimately ruled in 2019 that the Department acted “arbitrarily and capriciously,” and three of the four borrowers won their cases. However, the legal precedent remains that initial ECF approvals are not ironclad guarantees.

Fortunately, this risk is not uniform. The danger of a retroactive denial is heavily concentrated among non-501(c)(3) private nonprofits where their “public service” status is legally ambiguous.

If your employer is a clear 501(c)(3) charity or a government entity, your risk is significantly lower. However, if you work for a non-501(c)(3) organization with ambiguous eligibility, I highly suggest building a private savings buffer. Stash some cash in a high-yield savings account just in case your employer’s classification is ever challenged.

Finding PSLF-Eligible Jobs

If you are currently job-hunting rather than verifying a current employer, finding a qualifying role takes strategy. Unfortunately, there is no single database of all eligible jobs across the country.

As we discussed earlier, the employer type is the true test, not your job title. If you want to secure a federal role, USAJobs.gov is your best starting point. For state and local government jobs, look directly at your official state civil service website or municipal job boards.

Just remember to verify the specific legal structure and employee allocation of the hiring organization before you accept an offer. A tech startup with a social mission is not the same as a qualifying nonprofit in the eyes of the government.

Take Action Today

Do not leave your financial future and loan forgiveness up to chance. The bureaucratic hurdles are frustrating, but you have the power to protect yourself.

Use the employer search tool today. If the employer shows up as eligible, submit the ECF immediately. Don’t stop at the database check.

If you feel completely overwhelmed by a complex student loan situation, you don’t have to figure it out alone. For borrowers with edge-case employers or complex situations, you can book a consultation with me. We will review your specific loans and build a concrete plan to get you to 120 payments safely.

About the Author

Pedro Gomez is the new Student Loan Sherpa and a Certified Financial Planner™ with over a decade of experience helping clients navigate complex financial decisions. He is the founder of Global Financial Plan, where he writes about international living, geoarbitrage, and strategies for retiring young, and also leads Brickell Financial Group, a registered investment advisory firm focused on accelerating financial freedom.

Pedro is the architect behind the “12 Levels of Financial Freedom” framework and blends student loan strategy with long-term planning, tax efficiency, and investing. His work is especially geared toward upwardly mobile professionals, entrepreneurs, and those looking to design a life beyond the default path.

Pedro is available for strategy sessions and press inquiries.

The Credit Union I work for was started by law enforcement and the membership is law enforcement.

Would this help with the PSLF?

Great question. While your credit union’s roots in law enforcement are meaningful, PSLF eligibility hinges on who your employer is — not who they serve.

To qualify, the credit union would need to be either:

A government entity, or

A 501(c)(3) nonprofit that’s tax-exempt under section 501(a) of the Internal Revenue Code.

If your credit union is structured as a for-profit — even if it was founded by law enforcement and primarily serves that community — it generally wouldn’t qualify under current PSLF rules. You’ll want to confirm your employer’s tax status to know for sure.

If it is a 501(c)(3) or government-affiliated entity, then full-time employment there could count toward PSLF as long as all other requirements are met.

I work for a county government but the EIN does not show it as an eligible employer for PSLF. Can my county get certified for PSLF?

Absolutely. If your EIN doesn’t show up, the most likely explanation is that you are the first person at your employer to apply for PSLF. The EINs that show up as eligible are the ones where someone else has already successfully applied.

Is there anything I can do about my student loan which I have paid on time since 2011ish. The balance has not gone down. This loan will never be paid off. The capitalized interest is the reason. How is this fair to borrowers who take out federal student loans?

I worked for a credit union that was a non profit but Mohela doesn’t recognize the credit union as non profit. I can not get out from under this student loan. I have paid for it almost 20 years still with a balance of $70k. Do I need to seek counsel? I know nothing is life is fair but I also should be able to pay this loan off especially after almost 20 years.

It sounds to me like you might be closer to student loan forgiveness than you realize.

First, Credit Unions, though not-for-profit, don’t usually qualify for PSLF. There is a quick explanation on this page: https://studentaid.gov/articles/become-a-pslf-help-tool-ninja/ To get more technical: 501(c)(3) organizations all count toward PSLF, but Credit Unions are not 501(c)(3)s, because they are a different type of not-for-profit organization, the type of work they do is reviewed, and credit unions don’t meet that requirement.

However, given that you have been in repayment for over 20 years, you may be very close to IDR forgiveness. The one-time adjustment might help you get even closer, but the recent SAVE litigation might be a challenge. I’d encourage you to investigate IDR forgiveness and how it could help you.

Thank you!

I have a counseling company and would like to know if it is possible for me to become a qualified pslf employer?

If you made your company a 501(c)(3) not for profit entity, you could do it. Outside of that, there really isn’t an option.

When it comes to PSLF, the entity signing the paycheck matters far more than the work you do.