Most student loan borrowers realize that paying extra towards their debt will get the loans paid off faster. What many people fail to realize is the dramatic difference that just a little bit extra can make. This dramatic difference is especially true for people who are making minimum payments.

Borrowers struggling with student loan repayment can make an impact on their student loan debt by paying an extra $10 per month. The small additional payments can add up over the life of the loan enabling borrowers to save thousands and pay off the debt years earlier.

An extra $10 here and there won’t make thousands of dollars of debt disappear overnight. However, these small extra payments can speed up repayment and eliminate loans quicker than what lenders might prefer.

When Making Minimum Payments is a Challenge

Suppose you have many loans and can only afford the minimum payment on each of them. The debt seems like a lost cause, and you come to terms with the fact that you will just be making large student loan payments for the rest of your life.

Perhaps the most frustrating part of this situation is the fact that the vast majority of your payments are applied to interest rather than the principal balance. These payments that are almost entirely interest hardly put a dent in your loan balance and merely represent large profits for your lender.

The Value of a Little Bit Extra

Many borrowers are shocked to learn that at times over 90% of their payment is being applied to interest only. If you have a monthly bill of $100, $90 or more may become lender profit, while the small remainder reduces your loan balance.

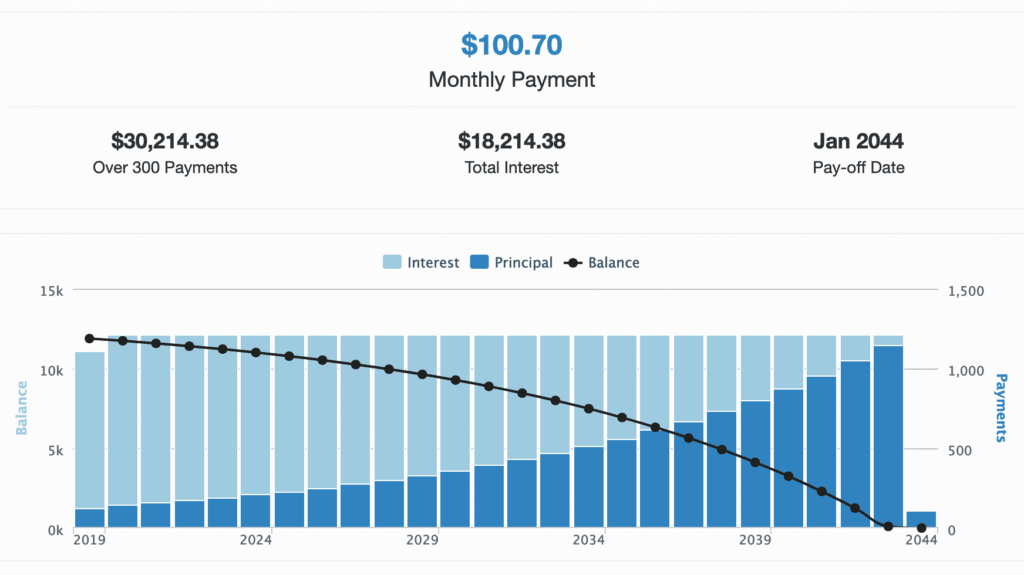

Take the example of a $12,000 student loan with a 9% interest rate on a 25-year repayment plan. The monthly bill on the loan is a reasonable $100.70, but of that $100.70, just over $10 will be applied to the principal on the first payment. Over the life of the loan, the borrower will spend over $30,000 paying back a $12,000 loan.

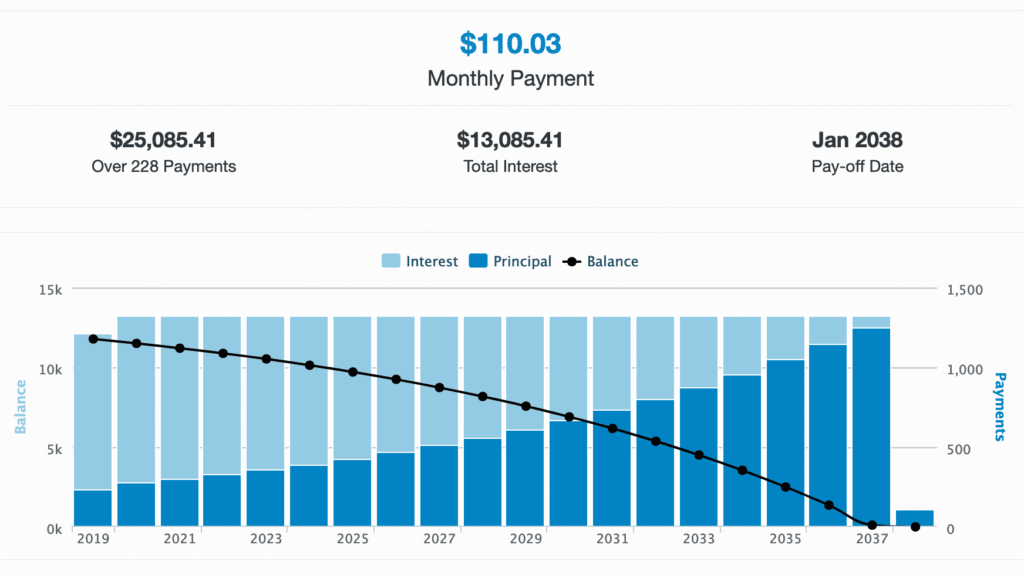

If you could pay $110 per month instead of that $100 per month, it might not seem like much, but it could fast-track your debt elimination. Instead of having your principal balance drop by $10 per month, it now drops by $20 per month. By paying $10 extra, you have doubled the monthly dent to your principal balance! If that extra $10 gets paid every month, the loan is paid off a full six years earlier.

The extra $10 per month saves over $5,000 in interest over the life of the loan!

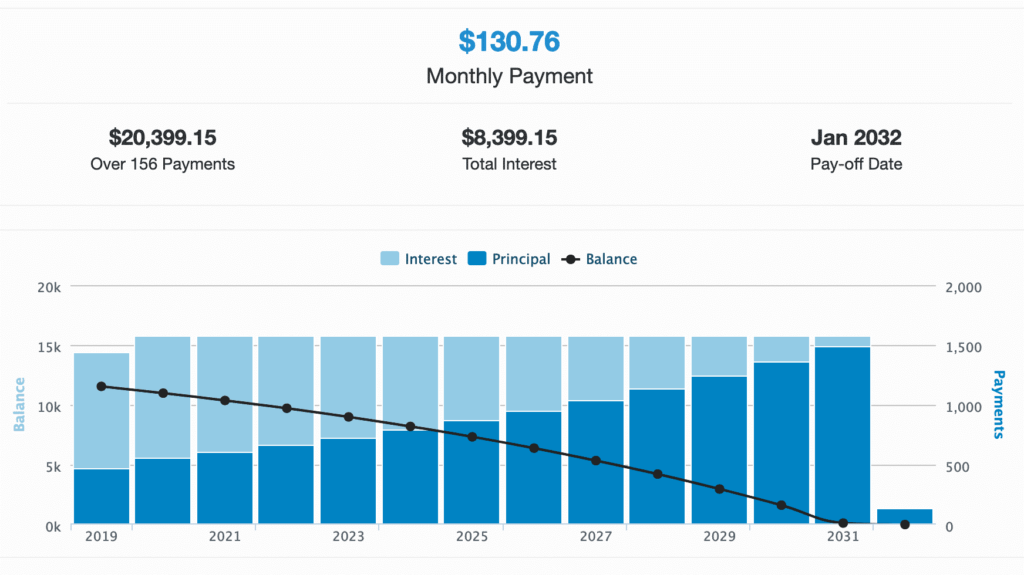

Better yet, if the borrower with this loan were to pay an extra $30 each month, the loan could be paid off in approximately half the time:

Many borrowers might think that double payments are required to pay the loan off in half the time, but in this example, we are paying $30 extra each month on a $100.70 student loan. Instead of taking 25 years to pay off the debt, we knock it out in 13 years. We also save nearly $10,000 in interest spending.

As you compare the three graphs, notice how there is more dark blue on each image. This is the spending on the principal balance. The light blue is interest… aka lender profits. By applying extra payments towards the principal balance, spending on interest is dramatically reduced.

Putting Together a Plan for Multiple Loans

The best way to eliminate student debt is to pay the minimum on all of your loans except one. For that one remaining loan, you pay it down as aggressively as possible.

From a math perspective, paying off the highest interest debt is the most efficient method. However, many people chose to pay off the smallest loan first, so that they can get a quick win and then free up some extra money each month to attack the next loan.

Regardless of whether you go after the smallest loan or the highest interest loan, you will start noticing results once that first loan comes off the books. At that point, you now have extra money each month that can be applied towards your other loans. With each loan eliminated, you can get more aggressive, and you have less debt.

The Key to Student Loan Elimination

The key to this whole process is to be able to pay just a little bit extra. In many cases finding $10 in your budget can put a noticeable dent in your student loans.

Being only able to afford the minimums across the board is a miserable experience. However, a small extra payment can have you on the path to debt freedom. If you can afford the minimum payment on all of your loans, you can afford to aggressively pay off your debt, even if it is only $10 at a time.

About the Author

Student loan expert Michael Lux is a licensed attorney and the founder of The Student Loan Sherpa. He has helped borrowers navigate life with student debt since 2013.

Insight from Michael has been featured in US News & World Report, Forbes, The Wall Street Journal, and numerous other online and print publications.

Michael is available for strategy sessions and to respond to press inquiries.

$10 extra per month is better than nothing extra at all! Slowly chipping away at principal can have huge benefits down the line!